I am a huge Thomas Friedman fan. As someone who has cousins from both Lebanon and Israel (thanks to the messiness of WW II and its impact on our family history), I simply adored From Beirut to Jerusalem. And he has been all over the impact of climate change and the world’s obligation to shift to renewable energy (see Hot, Flat, and Crowded). So when he published The World Is Flat in 2005, I lapped up his utopian vision of an integrated, globalized world.

But in retrospect, Friedman’s book was quite a bit ahead of his time. When reviewing the actual data, his description of a flatter world where ideas and capital freely flow, knowing no boundaries, simply did not pan out. Or at least, until COVID. After decades of stubborn roundness, the world has dramatically shifted – particularly in Startupland – to finally becoming remarkably flat.

A Flat World: Delayed Reaction

Friedman’s predictions, and those of other globalization enthusiasts, faced strong skepticism after the book’s publication. As economist Pankaj Ghemawat wrote in Foreign Policy in 2009 in an article titled “Why the World Isn’t Flat”: “The most astonishing aspect of various writings on globalization is the extent of exaggeration involved. In short, the levels of internationalization in the world today are roughly an order of magnitude lower than those implied by globalization proponents.” Examining a range of data sets — from global migration to foreign direct investment (FDI) — Ghemawat showed the extent to which globalization had, in reality, stalled.

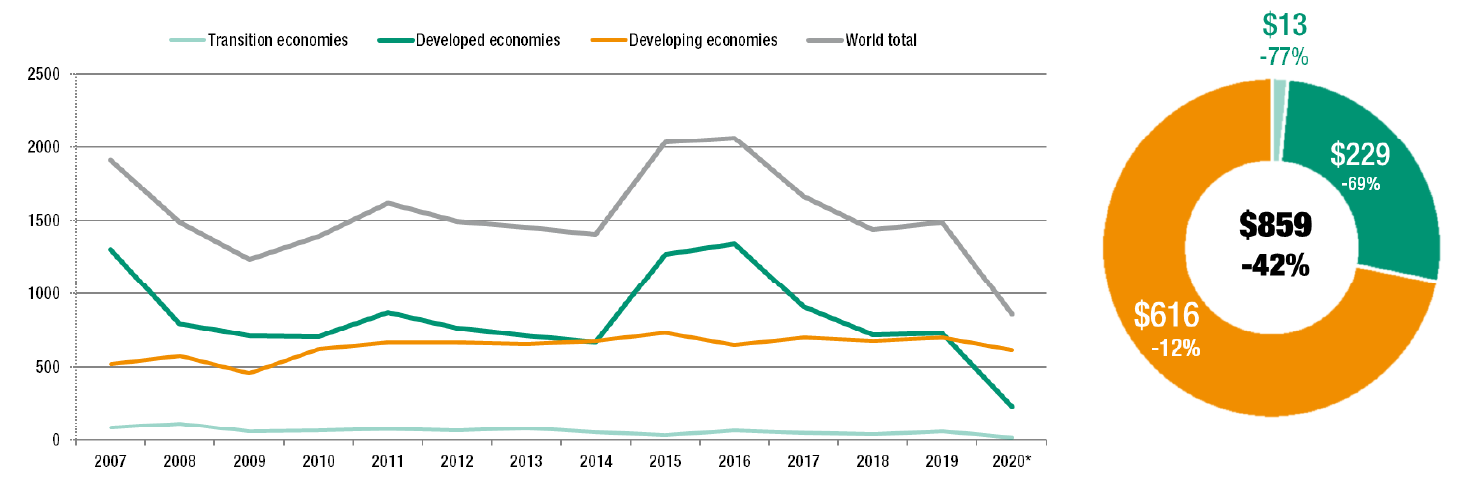

In the decade since Ghemawat wrote this criticism, many of these important measures have only gotten worse. FDI, for example, has actually gone down rather than up, as the chart below shows. As can be seen in the sharp dip in 2020, COVID may have accelerated digitization around the world, but it also slowed foreign investment and globalization.

In a recent article in The Economist covering the auto industry and its shift to electrification, I was struck by the fact that GM — still a powerful symbol of American industrial power — still derives 80% of its revenue from the domestic market, recently divesting its struggling operations in India and Russia. Hardly the outcome Friedman acolytes would have predicted 16 years after his declaration that a flat world would result in a “fundamental shift or inflection point” in how leading businesses would sit astride the globe.

Meanwhile, in Startupland: Flat, Flat, Flat

The odd thing, though, is that those of us in the venture capital (VC) industry are experiencing something on the ground completely different from what these figures and commentators suggest is happening in the mainstream economy. In fact, as VCs head into 2022 and continue to digest the implications of COVID on our operating model, I feel as if Friedman’s prediction of a flat world has finally arrived in full force in Startupland.

With the pandemic, geography suddenly no longer matters quite so much to either entrepreneurs or early-stage investors. Entrepreneurs can now easily access the investors who are the best fit for their venture in terms of specific expertise and value-add – and similarly, investors can now easily access entrepreneurs all around the world. Like many of our peers in the industry, the Flybridge partnership has become comfortable investing over Zoom in the last eighteen months.

Prior to making an initial investment decision, we often meet an entrepreneur only once in person to get to know them as a person and leader, and occasionally not at all. As a result, our geographic spread has changed dramatically. Previously, 40% of our portfolio came from each of NYC and Boston, where we have our two offices, while 20% of our companies were based outside these two cities. In contrast, in the last year, 75% of our new investments came from a wide variety of locations outside of these two centers, including the Bay Area, Denver, Los Angeles, London, Tel Aviv, Austin, Washington DC, Miami, as well as Cairo and Sao Paolo. Every single one of our colleagues in the VC industry is facing a similar, global expansion of geography — or dramatic “flattening”.

The vast majority of global venture capital is managed by US firms — according to the NVCA 2021 Yearbook, 67% of the $112B in global capital raised in 2020 was achieved by US firms (up from roughly 50% in 2015 and 2016). Thus, this greater comfort with geographic expansion by US firms is an important lever to drive more global startups to achieve success, which in turn will kick off a virtuous cycle and cause more global startups to attract more capital.

Global Unicorns: 2026

Although there has been a strong rise of global “unicorns” (i.e., a private company valued at over $1 billion), I would argue that this trend is only just beginning due to the shifting, COVID-induced investment patterns of VC firms. Because of the 5-10 year lag between when a company is first created and when it grows and matures to become a unicorn, we can expect to see a dramatic change in the number of global unicorns in, say, 2026. Comparing what the world looked like five years ago, in 2016, to today’s unicorn profile in 2021 might give us a few clues to help predict the 2026 outlook.

In December 2016, CB Insights indicated there were 183 unicorns (hat tip to the Wayback machine for helping me source this data), of which 55% were based in the US, 21% were based in China, and 24% were based in the rest of the world (ROW).

Today (in what is nearly December 2021), there are 848 unicorns (note: the CB Insights website indicates 887 but when one downloads their actual data set, they only have 848 categorized so there may be a data lag in the more complete categorization). Of these 848, 50% are based in the US, 19% in China, and 31% were based in ROW. Thus, a substantial, five percentage point increase in the share of “rest of the world’, despite the globalization trends remaining relatively tepid over the last ten years and despite the torrid pace of investing from the US-centric venture capital industry.

If we extrapolate five years from now into 2026 and assume that these trends continue, then we can posit that ROW will continue to gain in share and comprise of, say, 38% of the global unicorns. This figure is probably a very conservative one given the trends I highlighted earlier regarding the acceleration of US VC capital flowing outside the US. The chart below shows how this might play out in the coming years.

On a percentage basis, this figure sounds relatively modest — another five percentage points in five years. But on an absolute number basis, the implications are profound. If we assume that the rate of growth of unicorns continues at a similar pace in the next five years as it has over the last five years, we will see a total of nearly 4,000 unicorns in December 2026. If the ROW share of unicorns does indeed increase to 38%, then the total number of unicorns from the rest of the world will be an astonishing 1,493 — an increase of 1,233. If the share actually accelerates a bit, then the total number of new international unicorns outside of China will equal that of the US — despite the fact that US VCs manage two-thirds of the industry’s capital.

Unicorns or Bunnies?

The bottom line? In the coming years, US VCs — even small, niche ones like my firm, Flybridge — are learning to invest globally. As we make our first few investments in any individual country or region, our networks expand, our contextual awareness improves, and our comfort level for making the next new investment increases. As a result, international entrepreneurs are going to be able to attract US VCs in the coming years more easily than ever before.

And one final prediction — for those pessimists who think the unicorn herd is going to thin out in the coming years, think again. The unicorns are going to multiply so quickly in the next five years that we may start to think of them more like bunnies.