Each spring, I provide a comprehensive list of exciting, fast-growing, rapidly hiring startups that represent promising places to start (or continue) a career in Startupland.

This year, the theme in the innovation ecosystem is to leverage modern AI tools to drive productivity gains, in effect creating an army of 10x Founders and Joiners. As a result, hiring is more scarce. Software engineering job openings have hit a five-year low. At the same time, the AI wave is fueling amazing growth and opportunity. This list tries to capture where those specific pockets of opportunity lie for startup joiners.

The methodology for compiling the list remains the same: leveraging insider knowledge and input from VC and entrepreneur friends around the globe, we mix subjective and objective criteria in assembling the list. The objective criteria this year include:

Growth and momentum. Companies listed are growing revenue > 100% YoY (or > 50% for those of larger scale). In the AI market, where traditional revenue metrics can lag massive product adoption, some accommodations were made.

Hiring growth. This list is not valuation-driven but hiring-driven. Thus, we looked for companies that had grown headcount over the last 6, 12, and 24 months. The number and types of job openings were factored in.

Scale. Listed companies typically have> 50 employees. In a few cases, this threshold was relaxed to reflect AI superstars who are growing outrageously fast in other metrics, but doing so wildly efficiently (HT to the Tiny Teams Hall of Fame, who have achieved > $1M in revenue/employee, including our portfolio company BoldVoice).

Fundraising. In the Age of AI, fundraising is less important. Yet, building a massively valuable, enduring company still requires capital. We looked for companies that had raised > $50M in total capital with > $30M in the most recent round, ideally within the last 12 months.

Vintage. We biased the list to companies founded in 2013 or later.

We cover a wide range of geographies with the help of local VCs — Canada, Europe, India, Israel, MENA, LatAm, and SE Asia. Pitchbook and LinkedIn are important data sources, but less reliable outside the US, and so we are particularly grateful for the dozens of friends who shared their local market insights.

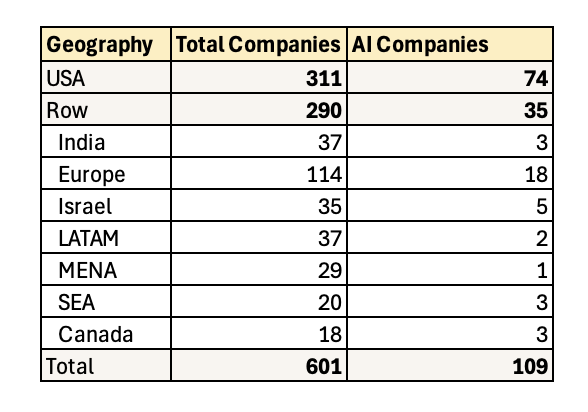

This year’s Rocket Ship List contains over 600 companies — over 300 US companies and just under 300 companies outside the US. 70% of the AI companies are based in the US. The geographic breakdown is here:

Although many companies remain remote-first, most large companies are once again geographically centered in one of the large global tech hubs. I advise my students to select and commit to a particular geography, as building a career in a community can be so rewarding for their careers and their lives (for my advice on securing a startup job, see my Joiner Playbook).

As usual, I am sure I have made many mistakes and omissions, and so thank you in advance for your feedback (comments below, please). A very special thank you to the indefatigable Vandit Gandotra of Harvard Business School, whose hard work and precision made this year’s list what it is.

Each Spring, I publish The Rocket Ship Startup List — a curated list of exciting, fast-growing, rapidly hiring private companies representing promising places to start or continue a career in Startupland. This year’s global list is comprised of over 570 companies in total — over 330 US companies and over 240 international companies.

Finding companies that are hiring isn’t easy, but after a few tough years, we are seeing some “green shoots”. The AI and climate sectors are white hot and once again, dozens and dozens of companies around the world are raising big rounds and growing rapidly.

The methodology for compiling this year’s list is similar to past years: I combine analytical sources like Pitchbook (financings) and LinkedIn (headcount, job growth, job listings) with insider knowledge and input from many VC and entrepreneur friends regarding who has real momentum. The mix of objective and subjective data from around the world helps assemble the list. Here are the objective criteria (not perfectly strict but roughly):

Growth/momentum: typically growing revenue > 100% year over year or > 50% for larger companies

Fundraising: typically has raised a total of > $50 million, including $30 million in the most recent round, which closed in the last 12 months.

Scale: typically > 100 employees (some AI companies are extraordinary in what they’ve achieved with very few employees, and so I relaxed this criteria more frequently this year)

Hiring: typically growing headcount > 30% year over year and have a robust number of job postings, including numerous entry-level positions that would be a fit for recent college or business school graduates.

Young: founded in 2013 or later

Note that this list is not necessarily “the best companies to invest in”. They represent “the best companies to pursue a job opportunity early in your career”. Thus, they must be hiring and I don’t care about their most recent valuation!

Once again, I want to profusely thank my numerous VC friends situated in startup hubs around the world for their input — including those in Canada (11 companies), Europe (92 companies), India (42 companies), Israel (31 companies), LatAm (32 companies), MENA (featured for the first time! 18 companies), and Southeast Asia (18 companies). Pitchbook is an amazing source of insight but there tends to be less reliable data outside the US.

We again included data from Glassdoor to provide insight into the “diversity and inclusion” score of a company since survey after survey indicates young professionals are more attracted to such companies (Glassdoor explains the importance and source of this data here and if you want more insight into hiring diverse talent check out Hack.Diversity).

Before reviewing the company list, I suggest checking out two of my previous posts where I provide detailed advice on how to select the right company and position yourself to secure a job — a playbook I have seen executed successfully now across my decades as a VC and entrepreneurship professor at HBS working with thousands of young professionals:

As usual, I am sure I have made many mistakes and omissions and so thank you in advance for your feedback. A special thanks to Amrut Rajkarne of Harvard Business School who did so much heavy lifting to make this year’s list as comprehensive as it is.

Without further ado, here is the Airtable link for the 570 companies.

570 Rocket Ship Startups for 2024

Disclosure: among the listed companies, the following are Flybridge portfolio companies — Amartha, FalconX, Finakargo, Habi, and Nasuni

Learn how the best startups iterate their way to success and find PMF faster than ever with the power of generative AI.

True to the experimentation mindset, I will be writing and iterating on the content in the coming months.

Subscribe to my newsletter, The Experimentation Machine, to read early excerpts, share feedback, and discover more opportunities to contribute.

I’m excited to announce that I am working on my next book: The Experimentation Machine: Finding Product-Market Fit in the Age of AI.

My goal is to create the essential guide for early-stage founders, offering a systematic, AI-augmented path to startup success. The methodology is based on the popular Harvard Business School course I’ve taught to thousands of students for over a dozen years, Launching Tech Ventures (LTV).

The book will be published at the end of the year.

I am constantly applying the frameworks I learned in Jeff’s course throughout my entrepreneurial journey, which includes launching an AI platform for investors.

Raghu Yarlagadda, co-founder and CEO of FalconX, a digital asset prime brokerage whose most recent financing was valued at $8 billion.

Build Your Startup as an Experimentation Machine

Many startups grapple with the elusive concept of product-market fit, often perceived as a nebulous, intangible “feeling” that only a few founders are lucky enough to stumble onto. This conventional wisdom is simply wrong.

The Experimentation Machine offers a rigorous, structured approach to defining and achieving success by outlining the clear steps that startups can take to transform product-market fit from an abstract concept into a tangible goal—-and how to use AI as a supercharged copilot. It will also feature case studies of real-world startup founders who iterated their way to success.

The main focus of the book will be to help founders define and answer three key hypotheses:

How to identify a “hair on fire” customer value proposition

How to build a scalable go-to-market sales and marketing engine

How to discover and deploy the optimal business model and pricing formula for sustainable growth

Using AI as a catalyst to test and iterate faster than ever before—almost like having an extra co-founder on your team

Despite some common misconceptions, entrepreneurship—and the precise processes that entrepreneurs execute on their path to success—can be taught.

Although I can’t guarantee a startup’s success, certain techniques—turbocharged by AI—can be applied to the entrepreneurial journey to dramatically improve the chances of winning.

The book is ideal for early-stage (pre-PMF) technology entrepreneurs, but it will also appeal to any startup founder or joiner, business students, and anyone who wants to learn the principles of entrepreneurship.

Alpha Readers Wanted

True to the spirit of the book, I will be running tests throughout the process. To that end, I am looking for ~50 “Alpha Readers” to join me.

Please let me know if you might be open to not only reading the first drafts of the book, but applying the lessons and frameworks to your own ventures and giving me tangible feedback on the concepts and frameworks.

If you are a founder, aspiring founder, or founding team member and interested in joining my Alpha Reader Group, sign up here:

Over our 22-year history, Flybridge has always focused on investing in trends that will define business and society in the future. In fact, our name is a nod to the highest deck on a boat, offering an unobstructed view of the waters ahead. From this vantage point, we scout for opportunities and look for ways to partner with Founders who are pioneering and shaping the future.

The future we see today is a world permeated by Artificial Intelligence. Today, there is no such thing as an Internet company. Tomorrow, there will be no such thing as an AI company. Every company will be an AI company. Our focus as a firm is solely to back ambitious Founders at the pre-seed and seed stages who are creating and building transformative companies for this AI-powered future.

We are not new to this space. Our first wave of AI and ML investments were in companies focused on using data to derive insights, allowing companies to improve decision-making. I wrote a cheeky blog post telling graduates to “Forget Plastics – it’s all about Machine Learning” in 2012, and we christened this cohort of companies as Full-Stack Analytics companies in 2014. Portfolio companies from this time include our 2010 seed investment in ZestAI, a pioneer in leveraging AI for Underwriting, and a 2011 pre-seed that we led in BitSight, an ML and data-powered pioneer in the Cybersecurity Risk Management market.

Our second wave of AI investments fell into the category of what we termed in 2019 as Applied AI companies. We noted that the application layer of AI ultimately drives the business value, but effectively doing so requires a deep understanding of the domain, the specific workflows that AI will seek to improve and optimize, and how best to incorporate AI into end-user experiences to engender trust and drive engagement. Portfolio companies operating within this thesis include Aiera, Bowery, Brighthire, Proscia, and Syrup.

Throughout both waves, we leveraged our long history of investing in infrastructure to back Founders building platforms to (1) manage and operationalize data and (2) make it easier for developers to build, deploy, and manage high-performance mission-critical applications. These investments include companies such as MongoDB, which we first backed in 2009 and which today is a leading company in the “AI Stack” with over $1.6B in annual recurring revenue (my partner Chip Hazard is still on the board, providing extremely useful insights into the sector), as well as other developer experience and “modern data stack” companies such as Firebase, FeatureLabs, Datalogue, and Stackdriver.

In the last 18 months, the capabilities of AI systems have taken a massive leap forward. A combination of technical advances drove this leap — the marriage of globally connected infrastructure, which created massive data sets upon which AI systems could train, exponential increases in computing power per dollar, and wildly sophisticated software techniques. These core foundations are joined with an unprecedented level of technical understanding, speed of advancement, and adoption by enterprises, developers, and consumers.

The future potential this creates exhilarates us, and, as a result, we no longer view AI as one of our investment sectors but rather our sole focus — the nucleus of the next industrial transformation.

Flybridge’s Investment Focus: Five Insights into the Future

We are looking to partner with ambitious founders building along one of five dimensions. While we believe every company will eventually become an AI company, in today’s world, an AI-powered company means more than just using AI as a supplementary tool. It implies that AI is a core element of the company’s value proposition and provides unique customer value. This integration means that AI is deeply embedded in the company’s primary product or service, significantly influencing its strategy and operational processes.

In the enterprise market, every Global 2000 company (and even small and mid-sized companies) will invest massively to build AI application stacks to drive competitive advantage. Analysts estimate that 2.5% of all enterprise software spending today is on AI applications – a level it took the SaaS industry nearly ten years to reach – a percentage that will likely grow 10x in the next several years. Fully realizing the power of AI within an enterprise requires a deep understanding of the domain and the specific workflows that AI will seek to improve and optimize and how best to incorporate this understanding to drive significant business value. Startups that can seize on this extraordinary surge in spending will do so on three dimensions: Vertical SaaS that is AI Native, Horizontal Applications that are AI Native, and Data Infrastructure and Platforms for AI Application Builders and Operators.

Vertical SaaS that is AI native. By building and providing fully integrated solutions that are purpose-built for vertical-specific industries, a new generation of SaaS companies that are AI native have an opportunity to carve out massive market opportunities, building on top of the rapidly evolving horizontal tools offered by big tech, emerging AI platforms for builders and operators, and the open source community. As more traditional software capabilities commoditize (driven largely by AI-powered co-pilots making it easier to develop applications), enduring and successful Vertical SaaS companies will not only streamline workflows but also generate the outputs and insights these systems previously enabled humans to perform. As a result, we believe that over $1 trillion in vertical SaaS revenue is “up for grabs” in the coming decade and are excited to back Founders participating in this transformation. Some AI-native Vertical SaaS companies in the extended Flybridge portfolio include Aiera, DayZero, Entr, Finkargo, Forcemetrics, H2Ok Innovations, Hansa, noetica, Porosity, Proscia, and Syrup.Successful Founders in this market will need to deeply understand customer requirements, build quickly, develop self-reinforcing data moats, and create unique value for their customers through well-designed user experiences that build trust, drive usage, and create new experiences that make individual contributors and teams far more efficient and effective. My colleagues Julia Maltby and Daniel Porras Reyes expanded on this here and here.

Horizontal Applications that are AI native. Artificial Intelligence promises to improve decision-making, streamline operations, and generate outputs and insights, but realizing this promise requires building these capabilities into an application. By providing functional capabilities that bring AI practices to horizontal workflows that cut across industries, Founders can help companies realize the AI vision of operational efficiencies while tapping massive TAMs that disrupt existing non-AI-native incumbents. We believe the discontinuous innovation that AI can introduce into the Horizontal SaaS market — expanding the market dramatically through increased automation — puts over $3 trillion in revenue “up for grabs” over the next ten years. Some companies building AI-native horizontal applications in the extended Flybridge portfolio include Brighthire, MelodyArc, Meritic, Quilt, Tato, and Teal.

Data infrastructure and platforms for AI application builders and operators. As a team, we have seen significant success supporting Founders who are building developer data platforms. These companies have typically seized upon massive technical shifts, for example, the rise of the cloud, to create platforms purpose-built for the new architectures, use cases, and deployment patterns. AI represents another such shift, and Founders creating solutions to make applications easier to build, run, manage, secure, and monitor will thrive. Not only will new applications emerge, but also the underlying models – especially if fine-tuned and open-source – and model infrastructure (vectors, knowledge graphs, etc) create a new part of the stack to be developed and managed. Further, as we know, AI models are only as good as their training data and how models apply inferences to data in a timely manner. As a result, for many customers, the AI journey begins at the data layer, and we believe companies building the “modern data stack” will see the same success in the coming AI application boom as those companies that make it easier to build, deploy, run, and manage these applications. Taken together, we believe these markets will exceed $200 billion in annual revenue within ten years. In addition to prior investments in companies such as MongoDB and Firebase, some of the companies building data infrastructure and platforms for AI application builders and operators in the extended Flybridge portfolio include Appwrite, Arcee, Avala, Blaze, FiveOneFour, 5x, Flojoy, Freeplay, Metaplane, Portkey, and Xata.

These first three areas will dominate the enterprise software market, disrupting incumbents who will race to keep pace with new capabilities and trends. Outside the traditional enterprise technology realm, we are excited about — and have actively been investing in companies — in two additional emerging areas.

AI-infused complex systems. In our Applied AI position paper published in early 2019 (here), we observed that in some cases, the best way to capture the value an AI-based system creates would be through selling a complete product or vertically integrated system. Each industry has different dynamics in this regard, but one example of the systems approach is Tesla selling autonomous EV automobiles versus providing autopilot or battery control systems to other OEMs. Given the dynamics of the auto industry and consumer preferences, a company could capture more value with a complete system (Tesla has a $780B market cap) versus being a vendor to the industry (Cruise was a billion-dollar acquisition). However, full systems companies in fields such as robotics have historically been challenging for seed-stage investors. They are complex — requiring multidisciplinary skills across engineering domains, hardware, software, and sophisticated AI, including adaptive control systems, vision, and perception systems – all of which make them more capital-intensive than we would like. This category of new systems has begun and will continue to change as many underlying building blocks, components, and models mature, and AI makes it easier to develop software. Many of these advancements come from the autonomous vehicle space, and Founders with this experience will be exceptionally well-positioned to apply their learnings to other domains where the systems packaging approach is the best way to capture value and meet customers’ needs. Some companies currently building AI Infused complex systems in the extended Flybridge portfolio include AeroVect, Alloy Enterprises, Agtonomy, BotBuilt, Bowery, Clockwork, DexAI, Glimpse, HaloBraid, Integral, and Intramotev.

AI native offerings. What are the out-of-the-box ideas for new products and services that don’t yet exist? In some ways, this question is the hardest one to answer — and yet represents exciting opportunities. Each new discontinuous platform shift enables creative Founders to build vertically integrated startups that have the potential to create entirely new industries. For example, Uber’s end-user value proposition could never be contemplated until virtually every potential customer had a GPS-enabled computer in their pocket or bag.

While enabling AI technology is advancing rapidly, translating this innovation into consumer value relies on human strengths – creativity, empathy, and intuition for user needs. Founders operating at this intersection of cutting-edge AI and human-centric design will thrive and create new categories and unforeseen applications we can not live without ten years from now. This intersection between advanced AI and insightful human design will lead Founders to redefine product utility, shifting existing paradigms to embrace new, more intuitive experiences. Some current companies in the Flybridge portfolio building to this future vision include BoldVoice, Decipad, Oasis, and Splice.

Conclusion: Just the Beginning

The step-change we have all witnessed in AI’s capabilities — from improving decision-making to achieving a level of cognition and task completion that rivals human benchmarks — is just the beginning. We are excited about the potential opportunities across all five dimensions in the coming decade.

If you are a Founder building to this AI-powered future, we want to hear from you!

This last semester, I ran a few generative AI experiments in my Harvard Business School (HBS) class. The largest experiment was the creation of an AI faculty co-pilot to help me teach my MBA entrepreneurship course, Launching Tech Ventures (LTV). This blog post will share some of the findings from that experiment.

Course Background

LTV is a course I created thirteen years ago in partnership with my colleague Professor Tom Eisenmann. This year, there were three sections of the course with over 80 Harvard MBA students each so a total of roughly 250 students. The course is taught using the case method and has a fair amount of analytical work associated with it. All the cases focus on pre-product market fit tech startups and put the students in the shoes of the founders who have to make difficult decisions with imperfect data that will make or break their startup.

As part of the course material, I have written over 50 HBS cases and teaching notes, two books, and numerous book chapters. There are also dozens of PowerPoint slide decks and Excel spreadsheets that we use in the course. Thus, there is a large corpus of material tied to the course that has built up over our thirteen years. I also created an online version of the course last year which required me to write out a precise transcript, including a detailed glossary of various frameworks and acronyms that the course covers, as well as a large number of video interviews with case protagonists. Finally, I’ve been writing blog posts about entrepreneurship for nearly 19 years. The importance of this large corpus will become clear shortly.

A final important background point about the course is that we have a course Slack and require our students to post reflections in Slack as part of their grade as well as use Slack to share various course materials. This use of Slack had several benefits: first, we have three years’ worth of Q&A content from the course Slack, and, second, Slack is emphasized as a part of the student workflow.

Building a Generative AI Chatbot: Chat LTV

With a small team, we developed a Slack-based chatbot called ChatLTV, which served as a faculty co-pilot throughout the semester. ChatLTV was trained on the entire corpus of my course — including all the case studies, teaching notes, books, blog posts, and historical Slack Q&A mentioned above — as well as selected and curated publicly available material. In total, the corpus contained roughly 200 documents and 15 million words.

We embedded ChatLTV into the course Slack in the form of a Slack app, allowing each of our 250 students to engage with the chatbot either privately or publicly. If the student chose for the engagement to be private, only the student and the faculty could see the interactions. If posted publicly, everyone in either the section or the full course could see the interaction.

Our technical approach was to respond to a student’s query by providing an LLM (in our case, we chose OpenAI’s ChatGPT v4) with two pieces of information: (a) the question being asked, (b) relevant context that the LLM can use to answer the question. The relevant context was retrieved from the corpus, which was stored in a vector database (in our case, we chose Pinecone). The most relevant content chunks were then served to the LLM using OpenAI’s API. This technique is known as Retrieval Augmented Generation (RAG) and is a useful way to improve the reliability and accuracy of the LLM’s responses. We used Langchain as a middleware tool to simplify the ChatLTV code base and take advantage of some useful services that sped up development.

An architecture for ChatLTV can be found here:

After a great deal of trial and error (see testing below), we settled on the following LLM prompt to provide an answer with the relevant chunked content as context: “You are a world-class algorithm to answer questions in a specific format. You use the context provided to answer the question and list your sources in the format specified. Do not make up answers.”

Since HBS has a copyright on much of the content being used, it was paramount that we ensure that the content would not flow into the public domain. Rather than using the OpenAI APIs directly, we used Microsoft’s Azure OpenAI Service for both development and production use. Leveraging Azure allows us to take advantage of the security, privacy, and compliance benefits, as well as guarantee that the data fed into the service is not used to retrain models that are then made available to others. The content is itself stored within the Pinecone Vector Database, which is SOC2 Type II compliant, and only relevant segments of content (e.g., a few paragraphs of a particular case or teaching note) are sent to the Azure OpenAI Service depending on the query that is made. During the course of our development, Harvard made a private LLM available to faculty and we anticipate porting ChatLTV over to it.

The total ChatLTV code base was 8000 lines for the backend (including 800 lines for RAG and 900 lines for content indexing, and then backend APIs, tests, and deployment code). We also created a content management system (CMS) that allowed faculty to add or delete additional content and observe student queries. That CMS was 9000 lines of code and a simple web-based application. The importance of the CMS will become clear later. The code was written over the course of the late spring and summer and took roughly 2-3 person months. If written today, with the rapid improvement in the underlying development tools, the code base would be substantially smaller (perhaps half the size) and the person months similarly smaller.

We also made ChatGPT4 publicly available to the students in the course Slack alongside ChatLTV. That way, students could use the public chatbot or the course chatbot, depending on their needs. In addition to providing the answers through Slack, the LLM shared the document sources for the answers in the Slack reply to the answer so that students could see the source material references.

Training and Testing the GPT, Adding Admin Content

Given the inherent probabilistic and nondeterministic nature of LLMs and the large body of text involved in the inputs and outputs, the development of an LLM app is an iterative process. We created numerous test data sets (roughly 500 Q&A queries) to manually test ChatLTV and provided an evaluation function to provide the development team with feedback on the quality of the responses.

We also ran an automated evaluation by using OpenAI to compare the outputs to the ground truth data and generate a quality score as well as manual testing noted above. The mix of manual and automated testing allowed us to play around with our prompts (i.e., prompt engineering) and content indexing. It also revealed an important feature that we later added: a repository of admin content. We realized in our informal user testing (i.e., discussions with prospective users, drawing from numerous students from past classes) that students would want to ask administrative questions about the course, such as “When is assignment #2 due?” and “How do I schedule office hours with Jeff?” and “what are the parameters for the final project?” Although this information is always provided to students over the course of a semester, students (shockingly!) sometimes forget the details and don’t know where to look for them. Thus, we created a set of content that we labeled “Course Admin” (e.g., “LTV Grading Rubric”, “LTV Writing Assignment 1”) and programmed the RAG algorithm to review that corpus first when providing answers.

Results: Student Experience

We launched the chatbot at the start of the semester in early September and used it throughout the semester, ending just last week. From my standpoint, the experiment was a smashing success. Throughout the semester, students found ChatLTV to be an invaluable resource for course preparation. They used the chatbot to ask clarifying and evaluative questions about case studies, analysis, acronyms, and a full range of administrative matters. Students expressed a high level of interest and excitement for the chatbot and described it as a valuable tool for enhancing their learning experience. A few quotes from a post-course evaluation:

I loved it — I found that I could use it to check my answers but more importantly understand if my methodlogy was directionally correct, which helped me get farther in my case prep. I loved that I could use it almost like a professor by my side as I worked through the questions, and I feel like it definitely helped me learn the content better.

It was nice to have a walled garden of content that we could know and trust to be used in tandem with other resources, including ChatGPT.

Over half our students — roughly 170 — made over 3000 queries over the course of the semester of ChatLTV. The course has 28 sessions, including 24 cases (versus exercises). Thus, there were roughly 130 queries made per case. When surveyed, nearly 40% of the students who used the chatbot gave it a quality score of a “4” or “5”. The usage and quality were frankly higher than I had anticipated. I was thrilled with both.

Interestingly, of the over 3000 queries, only a dozen or so were made using the public channel versus the private channel on Slack. Thus, 99% of our students elected for private queries with the chatbot rather than allow their peers to see what they were asking in advance of their case preparation.

Results: Faculty Experience

Perhaps most surprising to me over the course of this semester was the faculty experience. I had two fears: (1) ChatLTV would see no usage after all this work, or (2) students would use ChatLTV in a way that diminished the quality of the in-class conversation (e.g., getting “the answers” from the chatbot and spitting them back in a rote fashion). The latter was not at all the case. In fact, the quality of the in-class case conversation was excellent. Students appeared to have used the chatbot to prepare effectively for the case conversation and advance their understanding of the material, as noted in the student quotes above. When students provided answers to analytical questions that they were provided by ChatLTV, the faculty was able to push them to deconstruct their assumptions, methodology, and strategic implications rather than waste class time with “doing the math”.

Most interestingly, as a faculty member, I had a unique window into what my students were asking about before walking into the classroom. Each morning before class, I would inspect the admin CMS to see what queries had been made by what students (typically the night before — ChatLTV usage seemed to be most active between 10pm-2am!). From that resource, I had a unique opportunity to peer inside their minds and appreciate where they were at in terms of their comfort and knowledge of the material for that day and beyond.

A few examples will illustrate this point:

One student, let’s call him Jay, is an introvert. I didn’t see his hand up as much as others over the course of the semester. I wondered about his level of engagement with the material, but I was concerned that if I cold-called him, I would embarrass him because he was unprepared or lacking in command of the content. I noticed one morning that he had made numerous very thoughtful queries of ChatLTV about the day’s case. Based on the nature of my observation of the Q&A with the chatbot and his progression, I was confident I could cold call him that morning. I did. He crushed the opening, getting the class conversation off to a fantastic start.

I noticed that another student, let’s call her Nikki, was asking ChatLTV many clarifying questions before class. “What does OTE mean?”, “What does CPI mean?”, “What does WAU mean?” Nikki is a non-native English speaker and had previously worked at a Fortune 500 company, not someone who had been previously immersed in Startupland before HBS. Some of the acronyms may be hard for her to grasp and getting in the way of her learning journey. I asked ChatLTV in the public Slack channel to provide a list of the top 15 acronyms from the course and detailed definitions of each, which it accurately produced (thanks to the admin content glossary). As a follow-on, one wise guy student asked in the public chat for ChatLTV to come up with a catchy and funny way to remember the acronyms. Unfortunately, ChatLTV’s humor was not much better than “Dad jokes” level. Either way, I saw a subsequent reduction in Nikki’s acronym queries and instead more advanced, sophisticated queries.

Another student, let’s call her Mary, was frequently asking ChatLTV the morning before class to summarize the day’s case. I worried that perhaps Mary was not reading the cases and using the chatbot as a crutch. But I found her hand was up frequently and her comments were excellent, demonstrating command of the material. I asked her about it (in as nonconfrontational a manner as I could muster). She shared that because she was a young Mom, her sleep was highly variable and she was not in control of her time. To compensate, she prepared for cases many days in advance. The morning of the class, she liked to ask ChatLTV to help refresh her memory regarding the key case facts and issues so that she was ready to go each day. I no longer worried that Mary was taking shortcuts.

These and countless other examples demonstrated that ChatLTV was a useful tool not just for our students, but for me as a faculty member trying to meet my students where they were at any given moment to assist them in their individualized learning journeys.

Bonus: HBS LTV Project Feedback, a custom GPT

OpenAI launched a powerful new feature a few weeks ago, called custom GPTs. Using no code, Custom GPTs can create customized versions of ChatGPT, trained and tuned for a particular skill.

At the end of the semester (i.e., last weekend), I decided to create a custom GPT called “HBS LTV Feedback”, a critical academic evaluator to provide feedback on LTV final course papers and startup ideas. The final project requires students to apply a course tool to a startup of their choice, often their own, and write their reflections and takeaways from the experience.

Typically, students work in teams of two. Thus, with over 250 students, we will receive around 125 papers. We grade them all, but historically we simply don’t have the time to provide them with tangible written feedback on the quality of their paper or the quality of the idea. Thus, a custom GPT project evaluator.

It took me less than two hours to set up and train the custom GPT and zero lines of code. The functionality is ridiculously easy to use. As one of my genAI portfolio company founders likes to put it, “English is the cool new programming language for software.”

The results were excellent. I had to prompt the GPT to be tougher and more critical than its instincts might normally be (LLMs are way softer than HBS professors — in the face of widespread grade inflation, we still grade on the same forced curve from decades and decades ago). Students seemed happy with the results. Two feedback comments that were indicative:

Thank you so much for sending feedback. Honestly, will incorporate this feedback into the document ASAP since I am actually going to use this for real tests to validate the idea and business model over the next couple of months.

Thanks for the feedback and explanation – both human and in silico. A couple of the GPT points are pretty helpful! Especially the 2 areas for improvement for the project and startup idea.

One of my HBS faculty colleagues joked that this represented a historic moment as he believes no faculty in the 100+ year history of HBS has ever provided tangible, written, constructive feedback on final papers to each student. I don’t know if that’s entirely true, but using AI is going to make that much more routine and effective in the future.

Conclusion

This semester was a fun experiment. There is an enormous amount of usage of AI across the HBS faculty and curriculum and the school is racing ahead to embrace the tools even more on behalf of our students. Hopefully, this write-up will inspire other faculty around the world to run their own experiments.

Thank Yous

The ChatLTV project team consisted of Saswat Panda, Chiyoung Kim, Laura Whitmer, and Robin Lobo. Saswat was a total hero in writing every line of code. Special thank you to HBS’ administrative and IT leaders for allowing me to run this experiment and taking the risks associated with it, particularly Prof Mitch Weiss. Also thanks to my LTV faculty colleagues Lindsay Hyde and Christina Wallace. Finally, thank you to our 250 LTV students from 2023 as well as the 2000+ students who have taken the course over the last 13 years. None of us would be here if not for you.

The global SaaS market is measured to be $250 billion annually and still growing rapidly, as much as 20% per year according to some analyst estimates. Within the SaaS market, there is an increased focus on vertical SaaS – industry-specific or niche-focused functionality that follows the SaaS playbook. Remarkably, there are now nine public Vertical SaaS companies reporting more than $1 billion in revenue. These companies have captured tremendous opportunities by digitizing long-overdue analog industries or sleepy business processes.

For entrepreneurs and investors, vertical SaaS companies have been a goldmine of market opportunity. The combination of SaaS-like high gross margins (80-90%), recurring revenue (often net dollar retention rates exceeding 100%), and more efficient sales and marketing costs (pursuing focused, target markets) has consistently generated outstanding success. Some vertical SaaS companies capture over 40% of market share as compared to leaders in horizontal SaaS markets that struggle to hit 20%, leading to better pricing power and more attractive unit economics.

Vertical SaaS: Size Matters

Over the years, the knock against vertical SaaS is that market sizes have been too small to justify venture capital investment. However, two concurrent trends have recently dispelled this issue. First, market sizes have proven larger than originally projected, driven by dramatically accelerated technology adoption rates (see Crossing the Chasm Is Due for a Refresh). Given how impactful technology has been in creating competitive advantage in hotly contested markets, no company can afford to be a laggard. Second, vertical SaaS companies have successfully expanded their Total Available Market (TAM) by upselling additional products to their existing customer base.

The playbook for vertical SaaS is thus now well-understood: as a first act, establish a foothold in a niche with a tightly focused product distributed through classic early-stage go-to-market (GTM) techniques: find a few “lighthouse customers”, shape the product to meet their requirements, smother them with resources to help make them successful, and then use them as positive customer references in the market to attract others like them. Once a startup has integrated itself within an enterprise and its workflows and proven their indispensability, these companies can then proceed to extend their product portfolio to the same customers, typically offering follow-on products as well as some sort of fintech product. Eventually, vertical SaaS companies transcend point products and become true platforms and systems of record.

Vertical SaaS + Fintech Case Study: Toast

This strategy is commonly known as “SaaS + fintech” and a particular pioneer for this playbook was Boston-based Toast (NYSE: TOST), which has ridden this playbook to an $13 billion market cap. The company’s initial offering established a foothold through its point-of-sale order management software for restaurants – an approach many dismissed as too small a niche (including this foolish VC! 😜). As the company rapidly succeeded with this wedge product, the potential for more than just a single offering became clear.

As articulated by Bessemer partner Kent Bennett, who wrote in his Series A investment memo, “There are countless ways they can expand the product offering over time.” That forecast has proven prescient. The company has added to its “Lego stack” or “layer cake” of offerings with numerous fintech products such as payment processing and lending or credit (see figure below) – fueling a flywheel where both elements of their business model are proving to be accretive. In their Q1 2023 earnings release, Toast reported that of their $174M in gross profit, $71M came from their SaaS offerings while $150M came from their financial technology solutions (the company took a loss in hardware and professional services, making up the difference).

Flipping the Model: Fintech + Vertical SaaS

However, the classic Vertical SaaS + fintech playbook can be expensive to execute. Building an enterprise-ready SaaS product and creating an effective GTM motion – even in the age of product-led growth (PLG) – takes time and capital. This approach faces increasing challenges as markets and channels become cluttered, resulting in a more complex and expensive GTM – all at a time when the cost of capital has risen dramatically.

Further, the Vertical SaaS + fintech playbook was developed before the Age of AI. When the value of SaaS platforms was solely focused on workflow and business process optimization, the data collected was only marginally valuable. Today, the Age of AI means that AI is redefining vertical software. As my Flybridge colleague Daniel Porras Reyes writes, Vertical SaaS is becoming AI native, creating a powerful data moat as industry-specific systems and databases provide a powerful training set for machine learning models. The faster a company can acquire and leverage this proprietary data set, the better the models – and ultimate scale of the customer value proposition – will be.

Flybridge has thus developed an investment thesis that is an innovative approach to vertical SaaS. We seek companies that are flipping the standard playbook and starting with fintech as the first product offering and then develop the second or third act as a vertical SaaS platform. In other words, Fintech + Vertical SaaS instead of Vertical SaaS + Fintech.

Determining the sequence of products or services offered to your customers should be primarily guided by their specific needs, with a particular focus on addressing their greatest pain or “must-have” requirements. For instance, consider businesses that have a high demand for working capital. The optimal strategy to attract these customers might be to initially address their working capital challenges with a direct offering (“must-have”) rather than proposing front or back-office software solutions to improve their business processes (“nice to have”). By taking this approach, customers don’t have to justify new software expenditures, budget allocation, or prioritize valuable IT resources – all of which slow down buying processes and increase customer acquisition costs (CAC).

We believe companies can significantly diminish adoption barriers with a financial product as a “first act” and then later offer a SaaS product that gets embedded into their environment. By turning the classic vertical SaaS playbook on its head, startups can drive adoption up and CAC down, essentially using their fintech offering as a way to subsidize the CAC for their downstream SaaS products instead of the other way around. Further, a fintech-first approach eases the conversation with cost-conscious CFOs, who tend to be a major obstacle in enterprise sales.

Case Study: ZestAI

ZestAI is a technology company that uses AI software to automate and make credit underwriting more accurate. Flybridge was a seed investor in the LA-based startup and bought into a “flipped playbook” as part of the company’s vision: begin by lending capital to consumers off our balance sheet, collect data to train and fine-tune the credit models, and then spin out our own platform as a vertical SaaS offering that provides sophisticated, AI-driven underwriting for financial services firms.

The execution of this strategy has proven to take longer than we thought as we were early on the machine learning (ML) tools side (the company was founded in 2009!) and it took us time to pivot the organization and platform from B2C (directly lending to consumers) to B2B (selling an ML-based underwriting platform to financial services customers) as we ramped up an enterprise GTM organization from scratch. Operating in a heavily regulated environment didn’t help. Nonetheless, the company has seen tremendous success, doubled its customer base in 2022 after tripling it in 2021, and recently closed a $50 million growth financing (a rarity in late 2022).

Case Study: Finkargo

Another example of our flipped model thesis at work is our portfolio company Finkargo. The Colombia and Mexico-based startup has built a trade financing platform for international purchases serving small and medium-sized importers from Latin America. The company’s vision is to take advantage of the vacuum left by large banks in the region, using sophisticated underwriting technology based on import/export data to provide credit for SMBs, and then offer SaaS workflow software to connect importing SMBs with supply chain services and international suppliers, providing superior business intelligence and financial management.

For Finkargo, the sequencing of fintech + vertical SaaS was an attractive option given the industry and the market they are operating in. In LatAm, the credit crunch for SMBs is a massive opportunity as commercial banks are oligopolies with fat margins and little incentive to innovate or take risks. LatAm imports over $1 trillion annually, of which 40% is imported by SMBs (i.e., $400 billion). The company estimates that only 17% of these SMBs can access working capital. The credit crunch is even more acute with the growth in international transactions. Many companies in this category and region are family-owned, still operating with “pen and paper” or rudimentary spreadsheets, and are generally apprehensive about adopting technology solutions.

Imagine being an importer with a history of selling a product that has demand but cannot scale due to a lack of financing or cash flow mismatches. No front or back-office software value proposition is going to solve this pressing issue and jump to the top of your priority list. By offering importers new financing solutions, Finkargo has cracked the code on rapid adoption, resulting in a CAC payback of less than six months (unheard of in the world of SaaS), and building the foundation for a more comprehensive SaaS play.

Challenges to Fintech + Vertical SaaS

There are, of course, challenges to this Fintech + Vertical SaaS strategy that entrepreneurs need to overcome. In our experience, there are five major ones, detailed below.

Fintech is capital-intensive and requires capital sophistication. Although perhaps less expensive from an equity capital standpoint (if GTM can indeed be made more efficient), a fintech’s financing needs are quite different from the traditional path of Vertical SaaS + Fintech as providing working capital (lending), transfers (remittance), payment functionality, or insurance – four common fintech offerings – inherently requires capital. Thus, successful entrepreneurs who pursue this strategy need to be skilled at raising money from alternative capital sources at a low cost. Finkargo’s founder, Santiago Molina, is a sophisticated fintech founder who knew how to access low-cost capital and rapidly worked his way further down the cost curve as the data proved out the loan quality.

Building a fintech vs. SaaS culture and team. The operational and strategic differences in building a fintech vs. a SaaS startup are significant. Starting with a fintech-focused team requires a staff who understands and can operate in highly secure and complex regulatory environments. Sometimes it can feel as if fintech founders and SaaS founders and joiners (i.e., the early employees who join a startup) speak a different language. Fintech execs often come from traditional financial services industries (where suits, stare at balance sheets, and pay attention to the market and interest rate swings) while SaaS execs are trained in Lean Startup principles (and wear shorts, stare at no-code platforms to assist them with prototyping, and pay attention to the latest release of ChatGPT). The successful entrepreneur will find a way to merge these two cultures and skills into a single team with a shared mission. The two founders of ZestAI were ex-Google and CapitalOne. Merging these two cultures was not easy.

Prioritizing investments in software development. Fintech companies typically are more focused on the cost of capital as well as business process and financial systems integration rather than building great software products. Software investments in client-facing interfaces and building superior UI/UX capabilities will often get deprioritized. For a “flipped playbook” startup to achieve success, a long-term view on software development investments must be balanced with a shorter-term prioritization of fintech functionality, such as the flow of funds.

Fintech retention is harder, so don’t dawdle. When a startup chooses the Fintech + Vertical SaaS path, it is imperative to focus on a niche target industry, precisely define the Ideal Customer Profile (ICP), and deeply understand their pain points and requirements. As A16z put it: “While financial services can add a lot of value for customers, ultimately, a vertical SaaS company acquires and retains its customers because of its differentiated software, not the financial services it offers.” Thus, although an initial focus on a fintech offering is a shrewd go-to-market technique, it must be rapidly followed up with SaaS, even if the initial capabilities are rudimentary and unpolished. Finkargo’s initial SaaS functionality was basic and focused. Over time, it has become more robust and better designed as the company understands the supply chain workflows and use cases better by working directly with companies.

Raising money initially as a fintech. Another hurdle for a founder could be articulating their vision and securing funding when using fintech as the initial strategic focus. Investors value fintech revenue less highly than SaaS revenue for all the obvious reasons (non-recurring, lower gross margins, fewer economies of scale). Thus, public fintech comparables typically are valued at lower revenue multiples (2-4x) compared to SaaS revenue multiples (8-10x). As a result, founders need to be excellent fundraisers – painting a compelling and achievable SaaS vision. The goal is to persuade investors that, despite fintech being the primary short-term revenue source, the long-term business model envisages a significant portion of the revenue and margins eventually coming from SaaS.

For entrepreneurs who can master these challenges, we are enthusiastic about the opportunities that the flipped strategy Fintech + Vertical SaaS can bring.

Let us know if you are a founder taking this approach. We would love to hear more about what you are building!

For the past six months, there has been a lot of handwringing about the market downturn. Most everyone has been advising entrepreneurs to marshal their capital, cut costs, and extend their runway. In essence, play defense.

Many investors have been creating a whiplash effect with their portfolio companies. As one of my CEOs put to me, wryly — “In my January board meeting, I wasn’t hiring and scaling fast enough and told to ‘go, go’, go’. In my April board meeting, I was burning too fast and was told to ‘stop, stop, stop’.”

Her experience rhymes with many stories I’ve heard.

But recently, as the dust has settled a bit, I am seeing the best entrepreneurs realize that now is the time to play offense. The “play offense” playbook is well known to many, but hard to execute during a downturn. With the start of the football season around the corner (go Patriots!) and as I have been talking to my most talented entrepreneurs, I have been thinking more and more about what playing offense looks like in 2022–2023. Here’s the six-part playbook I’m hearing:

1) Talent acquisition. A few years ago, it was impossible to acquire talent. The best engineers, sales reps, and growth managers could name their price and had a dozen offers in front of them. Today, layoffs — particularly at growth stage companies — have led to a massive pullback in startup hiring. Thus, some of the most talented people in our ecosystem are suddenly up for grabs again. My best portfolio companies are judiciously adding remarkably talented people on the front lines, taking advantage of arguably the best talent market in a decade. I’m amazed at the quality of the hires that are happening for those who are seizing this moment to pursue outstanding talent.

2) Uplevel executive teams. It’s difficult to admit, but the executive team you were able to attract a year ago may be very different from the executive team you can attract today, particularly if you’ve grown in the last year and have a demonstrably bright future ahead. Like the talent point above, C-level executives at companies that were rocket ships at one point find themselves either laid off or disillusioned with their future prospects. That stretch VP of sales? Go get them. The COO who wouldn’t look twice at you a year ago, they’re begging to have the opportunity to re-engage. Rigorously evaluate the quality and capacity of your senior team and take advantage of the extraordinary executive talent looking for new homes and more promising pastures.

3) Process improvements. Let’s face it, the last few years have been frenetic. Velocity was at 11 for everyone. When you’re moving that quickly, inevitably there will be sloppiness in your execution. Sometimes it’s a gift to have the opportunity to slow down and fix your processes and make sure you’re doing things in a scalable, repeatable fashion. The Navy Seals have a saying, “Slow is smooth. Smooth is fast.” The best entrepreneurs are taking this slower moment to re-examine their key business processes and make sure that they’re running them more effectively and efficiently. Train your interviewers (Who has time for that?! Now you do!) and develop a more careful rubric for developing job descriptions and scoring candidates (sidebar: here is a complete guide to interview training from my company BrightHire). Rethink your product development prioritization process. Make sure sales best practices are being disseminated systematically within the go-to-market organization. Fire unprofitable customers — unsustainable, unprofitable growth is no longer valued. Executing well on this component of the playbook can provide significant leverage in a few short years.

4) Invest in your Product. Speaking of the product development process, if sales are less frenetic and customer requirements (and complaints) less noisy, take the time to invest in your product roadmap. Engineers and product managers love it when they’re “left alone”. Take the time to do deeper customer discovery and requirements gathering. Customers might be more open to participating in beta tests, new feature rollouts, focus groups, and customer advisory councils. This moment in time, where there are fewer distractions, is one where product teams can really make headway on their ambitious roadmaps and take the time to articulate — and take steps towards realizing — their long-term product vision.

5) Execute small, targeted M&A. Every asset was overpriced a year ago — houses, public stocks, startups. With the market correction, suddenly assets are more interesting to acquire. Many, many startups are flailing. Cash reserves are dwindling and they are desperate to find a safe landing. Thus, the companies that can afford to play offense have the opportunity to scoop up amazing teams, customer bases, and platforms. One of my portfolio companies has executed three acquisitions in the last six months at prices that are 2–3x lower than what the selling entrepreneurs were asking for a year ago. Developing skill as an effective acquirer is an important muscle for scaling companies and now is a great time to test out that skill.

6) Financing. There is a ton of money out there looking for great companies to invest in. Funds have raised an enormous amount of capital in the last two years. Never before in the history of entrepreneurship has there been this extraordinary amount of committed capital designated to invest in startups. If you have built a good business with promising prospects, you can stand out from the crowd far more easily today than ever before. Yes, your valuation may be 20–40% lower than you had hoped, but you can still raise plenty of money to buttress your balance sheet and execute more vigorously on steps 1–5 of the “play offense” playbook outlined above.

In talking to my best founders over the last few weeks, each of these elements of the “play offense” playbook is now well underway. The companies that can afford to execute on them, and do it well, will be lightyears ahead of their competitors in the next few years.

We are pleased to announce that Flybridge has raised a pair of new, oversubscribed funds with aggregate commitments of $150 million to continue our mission of backing ambitious founders at the pre-seed and seed stage. With this latest fundraise, Flybridge crosses $1 billion in assets under management, reflecting the outstanding success of our founders and portfolio companies during our 20-year history.

The new capital includes a $110 million Seed Fund (our sixth), which will invest in very early-stage startups leveraging the power of community as a source of competitive advantage, as well as an Opportunities Fund (our first), which will invest exclusively in our fast-growing portfolio companies as part of an outside-led growth financing. The Seed Fund has already closed eight new investments in AI/robotics, cybersecurity, low code/no code, creator economy, web3/crypto/NFTs, and SaaS. Our first Opportunities Fund investment was our recently announced investment in the Series B at Chief, a company we first invested in when we co-led the $3 million seed round in 2018.

The new funds complement our four Network Funds: (1) XFactor Ventures (focused on female founders), (2) The Community Fund (focused on under-estimated founders), (3) The Graduate Syndicate (focused on founders who recently graduated from Harvard), and (4) a new Network Fund called LTV Operators, comprised of C-level executives at unicorn startups.

A few years ago, we reinvented the firm and took an innovative approach to how we invest. Starting with The Graduate Syndicate in 2016, we created each of these Network Funds to empower operators and founders around the world to invest in talented founders from their own communities. While our core investment team is comprised of four partners and one senior associate, our fund is the anchor investor for each of these Network Funds that are made up of over 40 investment team members. We power the back office and handle fundraising while supporting these funds with mentorship, education, connections, and community. This strategy has both deepened our insights and expertise and expanded the Flybridge community in a massive way, allowing us to see 5x more investment opportunities than other seed funds of a similar size.

Ultimately, what really inspires our team every day is working with our community of over 400 founders across over 300 companies. They represent a very special, diverse group of extraordinary people who have invited us to join them in their disruptive missions to create significant companies from scratch. Some of these founders have become leaders in their industry — such as Bowery, Chief, FalconX, and MongoDB — and have done so with a unique blend of grit and passion.

While we acknowledge the range of crises rocking our world — from Ukraine to COVID to climate change to a racial reckoning — we could not be more bullish about the investment opportunities in front of us. At a time when we are collectively becoming increasingly digital, globally connected, awash in data, and decentralized, the number of innovations and disruptive opportunities is simply dizzying. Advancements in the science of entrepreneurship and company-building, as well as the accompanying tools, have dramatically compressed timelines and improved a founder’s odds of success. New companies can be created remotely and rapidly like never before. New products can be efficiently built upon powerful platforms that we barely dreamed of ten years ago. What will the next ten years bring?

We couldn’t be more excited to find out.

Thank you to our investors for their continued trust and a special thank you to our past, current, and future founders. We are honored to serve and support you.

The Flybridge Team Celebrating our 20 Year Anniversary in Miami

As many of you know, each spring I provide a comprehensive list of exciting, fast-growing, rapidly hiring startups that are promising places to start or continue a career in Startupland.

This year has been another boom year for tech startups, to say the least. As a result, it’s been the hardest list ever in my eight years of doing this. Graduating students and mid-career professionals have an abundance of opportunities to launch their careers. Leveraging insider knowledge and input from VC and entrepreneur friends regarding who has real momentum, I mix subjective and objective criteria in assembling the list. The objective criteria include:

Growth / momentum: typically growing users and/or revenue > 100% year over year

Fundraising: typically has raised > $40 million in the most recent round, which closed in the last 18 months (note: independent, private companies only! 10% of last year’s list went public and 3% were acquired)

Scale: typically > 100 employees

Hiring: typically growing headcount > 50%/year, including a number of entry-level positions that would be a fit for recent college or business school graduates

Young: founded in 2011 or later

With the help of numerous VC friends in startup hubs throughout Europe, India, Israel, and LatAm, I try to cover international startups each year. Pitchbook is less reliable outside the US and so I am particularly grateful to the dozens of folks who shared their local market insight. I left out China this year. That was a tough decision but because of the government’s anti-tech policies this year, it was hard for me to ascertain winners and losers with confidence.

This year, I include nearly 500 companies: 350 US companies and 140 non-US. As usual, the list is organized by location although I decided to be a bit more expansive in including startups from all over the US instead of just the tech hubs given remote and hybrid work. That said, even in this era, I advise my students to select and commit to a particular geography. Investing and contributing to a community in the long term is valuable for both your career and your life.

For the first time, we included a “diversity and inclusion” tab to the data set to guide prospective job seekers on whether this area is one of strength or weakness for the particular company. We used data from Glassdoor to populate this field (an explanation of the data source can be found here) and then translated that rating into three bands: weak, fair, and strong.

Before listing the companies, I suggest checking out two of my posts where I give more detailed advice on how to select the right company and position yourself to secure a job — a playbook I have seen executed successfully now across my decades as a VC and entrepreneurship professor at HBS working with thousands of young professionals:

As usual, I am sure I have made many mistakes and omissions and so thank you in advance for your feedback. Continued feedback (and lobbying!) definitely make this list better over time. A very special thank you to the talented Priya Bhasin of MIT Sloan whose precision and tenacity made this list what it is.

The AirTable for the 2022 Edition of the RocketShip Startup List

Disclosure: Among the listed companies, the following are Flybridge portfolio companies —BitSight, bloXroute, Bowery, Chief, EmCasa, FalconX, MadeiraMadeira, Splice, Tomorrow.io, and Zubale.

My usual daily obsession with new innovations, new entrepreneurs, and new fundings has been replaced with daily reports of bombs, convoys, and sanctions as Ukraine struggles for its survival. The blog post I had been working on regarding illiquidity in venture capital and the recent tech market correction now seems woefully tone-deaf.

My inbox and news feeds are full of heroic acts by Ukrainian friends, colleagues, and former students. One of my VC friends posted last night that he and his wife had flown from Boston to the Romanian border and handed out $7,000 in cash to 100 Ukrainian women.

This week’s NY Times The Daily podcast — “In Ukraine, the Men Who Must Stay and Fight” — described the buses being stopped at the Ukrainian border as all men ages 18–60 are ordered to remain in the country to take up arms to fight. As one Ukrainian young man put it, “Last week, I was contemplating what new game to buy for my PlayStation and today I am contemplating taking up arms to kill Russian soldiers and defend my country.”

A Ukrainian former HBS student who is a managing director of a private equity firm in Kyiv with over a billion under management, happily married with two young children, wrote: “All we have now fits in a few suitcases…this is not an abstract [classroom] discussion — it’s Munich all over again. We’re on the brink of WW III if the world doesn’t act. Please speak up. Please don’t remain silent.”

The echoes of 2022 and 1939 ring particularly true to my ears. My father was born and raised in pre-War Poland in an obscure city that is now in Western Ukraine called Lviv. I watch CNN every night, bewildered, as Andersen Cooper reports from Lviv. When the war broke out in September 1939, my father (then 14 years old — now turning 97 in a few weeks) and his sister and parents drove to the Polish-Romanian border, which today is near the very same Ukrainian-Romanian border town referenced above. Like my former student, they had crammed their most precious possessions into the few suitcases that could fit with them all in the car.

My father describes the September 1939 border crossing in his recently published memoir, “The scene at the bridge was unbelievable. The entire Polish government was evacuating. There was a long cavalcade of cars carrying various dignitaries from Warsaw. Some of the limousines flew foreign flags and carried officials from foreign allegations and their families…Poland and its most respected institutions were dissolving before our very eyes.”

My grandparents had doubted their decision to flee their friends, family, and home until they saw these dignitaries departing. They abandoned their suitcases, stuffed whatever they could fit into knapsacks, and walked across the border with the help of a smuggler and a healthy bribe — my grandfather handed over his precious silver pocket watch to the border guard. My father describes that his grandfather had the foresight to liquidate much of his net worth into a handful of bars of gold, one kilogram each, which he carried in his knapsack. As I read reports of modern-day Ukrainians carrying their cryptocurrencies across the border and the millions of dollars of donations flowing through the blockchain into the hands of Ukrainian families and relief organizations, I get the chills.

My father’s survival created a ripple effect, allowing him to eventually find his way to the United States, meet and marry my mother, and have me and my two sisters. I would not be here today if not for many random acts of fate during that harrowing time. Similarly, every single Ukrainian refugee has a story and a legacy. As the Talmud says, “Save one life, save the entire world.”

I pray for our leaders and I pray for the Ukrainian people and all those affected by this war.