AllSpice Co-Founder Valentina Ratner in front of Baker Library at HBS

This week, Valentina Ratner (formerly Toll Villagra), co-founder and CEO of AllSpice, announced the company’s $3.2M seed financing. AllSpice is essentially building “Github for hardware” — a collaboration hub inspired by software principles, powered by Git, and designed to accelerate hardware development. Apart from being a talented team with a unique solution targeting a significant market opportunity, AllSpice is consistent with our belief that community-driven companies that harness the power of a passionate ecosystem of members to drive adoption and growth will outperform. And they are executing on a go-to-market strategy that we love — emphasizing developer-driven adoption rather than top-down sales — a playbook successfully implemented at other Flybridge portfolio companies like MongoDB. We are #proundinvestors and look forward to working with Valentina, her co-founder Kyle Dumont (both of whom were in my Launching Tech Ventures class a few years ago), and the entire AllSpice team as they seek to realize their vision.

But this funding announcement isn’t our run of the mill portfolio company funding announcement. That is because AllSpice and Valentina are also the 100th company founded by a woman to join the Flybridge Community in the last five years. These 100 companies have been founded or co-founded by over 150 incredibly talented women.

Several years ago, we started asking ourselves some hard questions as we saw, again and again, the alarming statistics that ~ 85% of venture capital was going to male-only founding teams. Why was it that our firm and our community of founders were not much different than the statistics? Bluntly put, why were our potential investment opportunities so skewed towards companies founded by men?

We concluded that we were missing a massive opportunity to invest behind transformative companies founded by ambitious women. By missing out on these potential opportunities, we were missing out on generating incremental positive returns as we believe deeply that diverse founding teams will be more successful as they will be able to better access and retain talent, design better products and solutions to meet unmet needs in the market, and, ultimately, make better decisions, leading to stronger companies and better returns.

This conclusion led to the launch of XFactor Ventures in 2017, a pre-seed and seed-stage fund focused on women-founded companies pursuing billion-dollar opportunities cofounded by my talented partner Chip Hazard. To diversify our deal flow, we needed to diversify our network — you can’t invest in what you don’t see. XFactor allowed us to do this in spades. Each of the over twenty female founders who are now members of the investment team is a magnet for amazing companies, often with female founders. We also expanded our full-time investment team, adding Anna Palmer, who co-founded XFactor with us, and Julia Maltby. These changes have led to a dramatic difference in the gender balance of our deal flow and, slowly, our portfolio. Our portfolio company, Chief, is one example of a company that we believe is poised to generate outsized returns for our investors thanks to our commitment to this strategy.

XFactor Ventures I Team Photo

Chip has taken his decades of experience in venture capital and poured it into this mission, dedicating an enormous amount of time to creating a platform that would not only invest in more female founders but also train a new generation of female venture capitalists. Above is a photo from one of the first offsites of the original XFactor team. The three women in the back row are now general partners at VC funds — Erica Brescia (Redpoint), Aubrie Pagano (Alpaca), and our very own Anna Palmer.

We still have much work to do, but today is a day to celebrate a small victory along the journey: 100 new companies founded by women, the launch of an amazingly promising company in AllSpice, and a ripple effect that we look forward to seeing in the market for many years to come.

And a special thank you and hat tip to my partners, Chip and Anna, for leading the way.

Over the holidays, there was a bit of a firestorm on Twitter over comments made by venture capitalist Joe Lonsdale of 8VC regarding VCs and racism. The original tweets and resulting dialog inspired me to write this post in an attempt to address the question that was posed: how do we explain the fact that only 1% of VC capital goes to Black founders? “Are VCs racist?” Or perhaps a better-framed question, “Why is there such a persistent race gap in the VC industry?” As we look ahead to 2022, I believe this issue is one of the most important ones that our industry needs to grapple with.

For context, I have been examining the systemic biases in the tech industry for a number of years as a result of three hats that I wear. First, through my day job as a practicing venture capitalist — I cofounded a NY and Boston-based early-stage VC fund, Flybridge Capital roughly 20 years ago. Second, through my civic work at Hack.Diversity — a workforce development nonprofit I co-founded six years ago that provides a pathway for young Black and Latinx professionals into the tech ecosystem. And finally, through my part-time work as a member of the faculty at Harvard Business School where I recently created a course with my colleagues Professors Henry McGee and Archie Jones called Scaling Minority Businesses, a field course where we study the impact that systemic racism, lack of access to capital, and lack of access to customers has on minority-owned businesses.

I am not a scholar in the field of systemic racism and bias. Instead, I am an intellectually curious practitioner and a white male of privilege trying to learn about these issues and through that learning, apply them to change a pernicious injustice in our startup ecosystem. It’s a journey and I know I have more work to do, as do the institutions that I’m a part of.

Beyond correcting these injustices, I have also been studying this area in an attempt to be a better investor. Over the years as I’ve read and discussed these issues, my thinking has changed. Once you lift the veil on all of the unconscious biases and racist systems that require dismantling, it’s hard to see the world the same way. But I am also seeing some amazing progress and emerging leaders who are successfully challenging the status quo and changing this system one brick at a time.

Joe Lonsdale’s Tweets

So with that background, let’s dive in. First, let me share the tweets that Lonsdale posted. The first one was in response to a tweet from a venture capitalist and entrepreneur named Prince Ramses (@imthedronelord):

Lonsdale later deleted that tweet but followed it up with another two that I’ll include here in response to a thoughtful reply from Steve Ekechuku, a NY-based lawyer:

There were a number of other tweets in the subsequent back and forth, but I’ll stop here for now as I think these three capture the essence of the comments that sparked the controversy.

I should state upfront that I don’t know Lonsdale. Although we are in the same small industry, we have never met. Reading his tweets really upset me. And I can’t even imagine how upsetting they were for Black VCs and entrepreneurs. That said, I want to try to turn the incident into a “teachable moment” and broaden the conversation to examine the three biggest contributors to the race gap in VC funding.

1. Systemic Biases (Largely Unconscious) and Discrimination

Each year, Flybridge chooses a non-business book to send to our founders as a year-end gift. This year, we chose an influential book in social psychology called Blindspots: Hidden Biases of Good People. The authors, Professors Anthony Greenwald of the University of Washington and Mahzarin Banaji of Harvard, build on their pioneering work in creating the Implicit Association Test (IAT) to demonstrate that human beings have strong, often unconscious and instinctive, biases. In research study after study, the authors describe these remarkable “mind bugs” that show how our unconscious preferences manifest themselves in strange, surprising and sometimes disturbing ways.

The implications of this social psychology insight are powerful in the context of racial discrimination. Although the authors indicate that various studies show that we have seen explicit, overt biases decrease in America in recent decades (I should note that the book was published in 2013 — years prior to the Trump era and the recent rise in hate crimes), strong implicit biases remain. Specifically, the IAT has “revealed that approximately 75% of Americans display implicit (automatic) preference for white relative to Black.”

Towards the end of the book, the authors conclude that these hidden biases “plausibly contribute more to discrimination in America than does the overt prejudice of an ever-decreasing minority of Americans.” In their appendix, they frame that “Black Americans experience disadvantages — meaning inferior outcomes — on almost every economically significant dimension. This includes earnings, education, housing, employment, status in the criminal justice system, and health.” And they acknowledge that there are two theories of Black disadvantage. Again, quoting from the appendix: “One set of theories credits Black Americans themselves with full responsibility for the disadvantages they experience. The other set…place the entire responsibility elsewhere.” The authors conclude that “institutional discrimination as a cause of Black disadvantage is undeniable historical fact.”

I believe this book contains important implications for our startup ecosystem. The authors’ insight that “human judgment and behavior is produced with little conscious thought” is illuminating in the context of investment and hiring decisions. In Startupland, these decisions are made with a modest amount of data and in the context of a large number of complex variables. Thus, instinct is a powerful force in decision making and instinct is rife with biases, both conscious and unconscious. Pattern recognition can be used as a weapon in startup pitches by founders. I once had a young entrepreneur kick off our pitch meeting by sharing that he was a Harvard dropout. I later found out that he actually never attended Harvard College and never dropped out. Instead, he enrolled in a few Harvard extension school courses, which are open to the public, and then ceased enrolling in the extension school. Obviously, he was trying to anchor me and my unconscious mind on famous Harvard dropouts like Bill Gates and Mark Zuckerberg, using the power of association to create a favorable impression of his founder journey. This example is somewhat harmless (I didn’t fall for it), but it’s emblematic of how unconscious, positive associations towards some founders and negative towards others can affect investment decision-making and lead to less capital going towards Black founders.

Another terrific book by NYU Professor Jonathan Haidt demonstrates that these biases are inherent in humans, very natural, and very hard to deconstruct. The Righteous Mind is a book that Haidt, another social psychologist, wrote to explain tribalism in politics but I read it through the lens of a venture capitalist and what it said about our ecosystem. Like Greenwald and Banaji, Haidt reviews the extensive research and philosophical underpinnings that show that humans are fundamentally intuitive decision-makers. His work is more focused on moral judgments and the insight that moral judgments are unconscious and that these unconscious cognitive processes are evolutionary in nature, allowing us to form social groups and tribes. This rapid intuitive judgment is a powerful force that is then followed by rationalization. As Haidt points out, “the intuition launched the reasoning, but the intuition did not depend on the reasoning.”

If these two books are right, we should see evidence of these unconscious biases in investor decisions. Not surprisingly, a few recent studies have shown exactly that.

2. Intuitive, Biased Investment Decisions: Gender and Race

In 2017, four researchers (including my colleague Professor Laura Huang) published a ground-breaking article in Harvard Business Review that observed Q&A interactions between 140 prominent VCs and 189 entrepreneurs that took place at TechCrunch Disrupt New York. When they analyzed the Q&A sessions, they saw that VCs asked different types of questions to the male founders than they did to the female founders. VCs “tended to ask men questions about the potential for gains and women about the potential for losses.” Surprisingly, the researchers found evidence of this bias with both male and female VCs! Not surprisingly, entrepreneurs that are asked promotion-based questions raise more money than those asked prevention questions. In other words, male and female VCs had similar intuitive biases about the male and female entrepreneurs they met with, resulting in more capital going to male entrepreneurs.

In 2019, Stanford Professor Jennifer Eberhardt and colleagues published another study demonstrating the unconscious biases of asset allocators. By creating fictitious VC fund manager profiles and asking prospective limited partners (LPs) to evaluate those profiles, the researchers showed that LPs were unable to properly assess Black-led VC managers or distinguish between the stronger and weaker, Black-led teams. Professor Eberhardt concludes, “One explanation of this finding could be that investors rarely see Black-led teams. They simply don’t know how to evaluate them.” (I should note that Professor Eberhardt also recently wrote a book on hidden biases: “Biased: Uncovering the Hidden Prejudices That Shapes What We See, Think, and Do”. I haven’t read it yet, but it’s on the list!).

These studies are manifestations of substantive racial biases in our ecosystem — perhaps some of these lead to overt racism but, in my opinion, and based on the research, even good people who are not racist also demonstrate unconscious and instinctual biases.

Black VCs and entrepreneurs don’t need academic studies to tell them what they experience day to day. Venture capitalist and entrepreneur James Norman wrote a compelling HBR article called, A VC’s Guide to Investing in Black Founders in which he discusses differences between Black and white founders. These differences can lead to different profiles, paths, cultures, and styles of communication. As Norman points out, “Unfortunately, you can count on one hand the number of investors who have first-hand experience with our journey, and there are only a handful more investors that look like us.” (disclosure: Norman launched a new VC fund called Black Ops VC where I’m a personal investor).

3. Historical, Systemic Racism and the Wealth Gap

Continuing Norman’s theme, we now turn to the second powerful force that leads to the “1% problem” — historical, systemic racism and the wealth gap. When researchers and historians examine the economic implications of systemic racial biases as manifested in policies, the scorecard is pretty damning. Brookings scholar Andre Perry wrote a powerful book reviewing this history called Know Your Price: Valuing Black Lives and Property in America’s Black Cities. In the book, Perry builds on previous work by some of his Brookings colleagues in measuring the Black-white wealth gap — where the average Black household has $17,600 in median net financial worth as compared to $171,000 for the average white household — and outlines the underlying factors that have led to this disparity. Perry reviews policy decisions around redlining and housing, urban development, disparities in schools, health care, and incarceration policies to demonstrate the uneven playing field that Black households have faced in recent decades.

For more on housing policy, in particular, I also highly recommend Berkeley Professor Richard Rothstein’s seminal book on redlining and housing — a critical source of household wealth for Black and white households in recent decades — called Color of Law: A Forgotten History of How Our Government Segregated America. These two books as well as many others (e.g., Keeanga-Yamahtta Taylor’s How Banks and the Real Estate Industry Undermined Black Ownership) provide a glaring picture of policies that have consistently held back economic development for Black businesses and families, thereby reducing the opportunity for generational wealth creation. Linking the impact of these policies on the 1% problem is clear, for example:

Black families have dramatically less wealth so young Black professionals from those families take on less risk early in their career when they are still establishing themselves and paying down their loans.

Friends and family money to support very early company formation is more plentiful in white families than Black families.

Professional networks with access to early-stage capital are more available to white professional networks than Black professional networks.

Black professionals don’t have easily accessible friends and family ties to the industry because the industry is small and closed.

With so few allocators of capital being Black (one analysis by my colleague Professor Josh Lerner showed that only 1.3% of assets under management are controlled by substantially and majority diverse-owned firms, which include women and minorities), with the important role of pattern recognition and intuition in decision making, and with the historical systemic policies and practices that have led to dramatically lower levels of wealth in the Black community, it is no surprise that we are where we are with only 1% of funding going to Black entrepreneurs.

The arguments above suggest that it is not because VCs or even LPs are overtly racist (although I acknowledge that some are and many Black founders and VCs have shared some pretty bad stories of encounters with them). Like many other humans, they’re highly biased decision-makers operating in the context of a historically racist system. Unlike many other humans, those biased decisions have massive economic consequences.

What Are The Solutions?

Hedge fund manager Howard Marks famously observed that the best investments come from nailing a theme or bet that is non-consensus. That’s why Flybridge has intentionally pursued a series of strategies in recent years to increase our investment in more female founders (see XFactor Ventures) and founders of color (see The Community Fund, where we are seeking to add a few new partners): we believe we are going to find amazing investment opportunities that others are missing. And it’s why I’ve been personally investing in more Black VC managers, such as Black Ops VC, Visible Hands, Collab Capital, Stellation Capital, and others — these managers and others like them are seeing attractive investment opportunities that I am not seeing and don’t have access to. There is much more we can and will do in the coming years. And I hope that other VCs and LPs follow the opportunity and direct more institutional and personal capital to underrepresented VC managers.

Fortunately, there are promising efforts underway to get more capital in the hands of emerging Black managers as well as Black founders — initiatives that, critically, are breaking open the small coterie of insiders that control the industry. Many are being driven by LPs (who are allocating capital to Black founders and asking hard questions of non-diverse managers), by entrepreneurial VCs (who are creating both new funds and changing the culture and processes of big firms from within), and by founders. Successful founders have tremendous power in this industry. I hope to see more founders creating wildly successful companies led by diverse teams. But I also hope to see all founders demand that their cap tables and board rooms contain diverse leaders.

These efforts and the rise of strong, talented emerging Black managers (e.g., Precursor Ventures, MaC Venture Capital, Harlem Capital, Backstage Capital, RareBreed VC, and many more as well as the ones mentioned above) give me hope that we are seeing a sea change in our industry. It will take years to play out — largely because of the unconscious biases, historical racism, and friction points mentioned above — but I’m hopeful that we won’t be talking about the 1% problem in ten years. And I sure hope that we won’t see other powerful and prominent VCs making hurtful proclamations that inappropriately attack or blame Black people and culture for the funding gap. The story of the coming years is more likely to be the rise of many wildly successful entrepreneurs and investors from backgrounds, cultures, and countries that we have not seen before.

We all have a role to play in helping facilitate that outcome. My hope is that in so doing, we will finally achieve the dream of leveraging the power of all the talented humans on this planet eager and ready to innovate.

Many thanks to the many friends and colleagues who provided me with valuable insight and input for this post, including each of my Flybridge colleagues (Anna, Chip, Jesse, and Julia), Daniel Acheampong, Kwesi Acquay, Jewel Burks Solomon, James Norman, Jody Rose, Ed Zimmerman, and many of my brilliant HBS students.

I am a huge Thomas Friedman fan. As someone who has cousins from both Lebanon and Israel (thanks to the messiness of WW II and its impact on our family history), I simply adored From Beirut to Jerusalem. And he has been all over the impact of climate change and the world’s obligation to shift to renewable energy (see Hot, Flat, and Crowded). So when he published The World Is Flat in 2005, I lapped up his utopian vision of an integrated, globalized world.

But in retrospect, Friedman’s book was quite a bit ahead of his time. When reviewing the actual data, his description of a flatter world where ideas and capital freely flow, knowing no boundaries, simply did not pan out. Or at least, until COVID. After decades of stubborn roundness, the world has dramatically shifted – particularly in Startupland – to finally becoming remarkably flat.

A Flat World: Delayed Reaction

Friedman’s predictions, and those of other globalization enthusiasts, faced strong skepticism after the book’s publication. As economist Pankaj Ghemawat wrote in Foreign Policy in 2009 in an article titled “Why the World Isn’t Flat”: “The most astonishing aspect of various writings on globalization is the extent of exaggeration involved. In short, the levels of internationalization in the world today are roughly an order of magnitude lower than those implied by globalization proponents.” Examining a range of data sets — from global migration to foreign direct investment (FDI) — Ghemawat showed the extent to which globalization had, in reality, stalled.

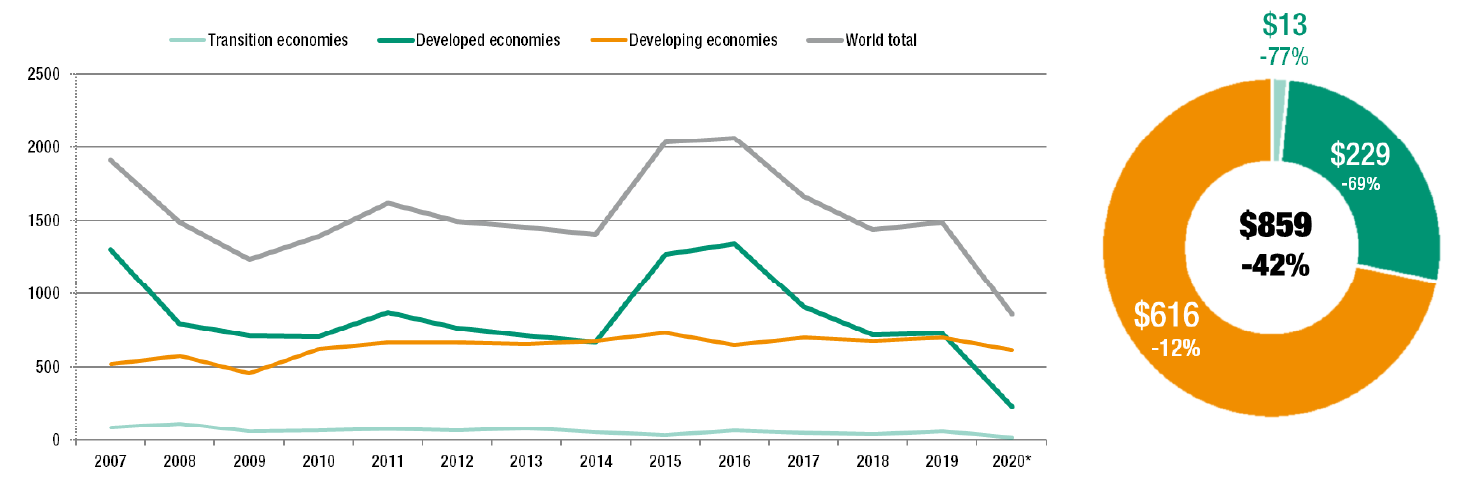

In the decade since Ghemawat wrote this criticism, many of these important measures have only gotten worse. FDI, for example, has actually gone down rather than up, as the chart below shows. As can be seen in the sharp dip in 2020, COVID may have accelerated digitization around the world, but it also slowed foreign investment and globalization.

Surprisingly, Foreign Direct Investment has been flat to down for the last 15 years.

In a recent article in The Economist covering the auto industry and its shift to electrification, I was struck by the fact that GM — still a powerful symbol of American industrial power — still derives 80% of its revenue from the domestic market, recently divesting its struggling operations in India and Russia. Hardly the outcome Friedman acolytes would have predicted 16 years after his declaration that a flat world would result in a “fundamental shift or inflection point” in how leading businesses would sit astride the globe.

Meanwhile, in Startupland: Flat, Flat, Flat

The odd thing, though, is that those of us in the venture capital (VC) industry are experiencing something on the ground completely different from what these figures and commentators suggest is happening in the mainstream economy. In fact, as VCs head into 2022 and continue to digest the implications of COVID on our operating model, I feel as if Friedman’s prediction of a flat world has finally arrived in full force in Startupland.

With the pandemic, geography suddenly no longer matters quite so much to either entrepreneurs or early-stage investors. Entrepreneurs can now easily access the investors who are the best fit for their venture in terms of specific expertise and value-add – and similarly, investors can now easily access entrepreneurs all around the world. Like many of our peers in the industry, the Flybridge partnership has become comfortable investing over Zoom in the last eighteen months.

Prior to making an initial investment decision, we often meet an entrepreneur only once in person to get to know them as a person and leader, and occasionally not at all. As a result, our geographic spread has changed dramatically. Previously, 40% of our portfolio came from each of NYC and Boston, where we have our two offices, while 20% of our companies were based outside these two cities. In contrast, in the last year, 75% of our new investments came from a wide variety of locations outside of these two centers, including the Bay Area, Denver, Los Angeles, London, Tel Aviv, Austin, Washington DC, Miami, as well as Cairo and Sao Paolo. Every single one of our colleagues in the VC industry is facing a similar, global expansion of geography — or dramatic “flattening”.

The vast majority of global venture capital is managed by US firms — according to the NVCA 2021 Yearbook, 67% of the $112B in global capital raised in 2020 was achieved by US firms (up from roughly 50% in 2015 and 2016). Thus, this greater comfort with geographic expansion by US firms is an important lever to drive more global startups to achieve success, which in turn will kick off a virtuous cycle and cause more global startups to attract more capital.

Global Unicorns: 2026

Although there has been a strong rise of global “unicorns” (i.e., a private company valued at over $1 billion), I would argue that this trend is only just beginning due to the shifting, COVID-induced investment patterns of VC firms. Because of the 5-10 year lag between when a company is first created and when it grows and matures to become a unicorn, we can expect to see a dramatic change in the number of global unicorns in, say, 2026. Comparing what the world looked like five years ago, in 2016, to today’s unicorn profile in 2021 might give us a few clues to help predict the 2026 outlook.

In December 2016, CB Insights indicated there were 183 unicorns (hat tip to the Wayback machine for helping me source this data), of which 55% were based in the US, 21% were based in China, and 24% were based in the rest of the world (ROW).

Today (in what is nearly December 2021), there are 848 unicorns (note: the CB Insights website indicates 887 but when one downloads their actual data set, they only have 848 categorized so there may be a data lag in the more complete categorization). Of these 848, 50% are based in the US, 19% in China, and 31% were based in ROW. Thus, a substantial, five percentage point increase in the share of “rest of the world’, despite the globalization trends remaining relatively tepid over the last ten years and despite the torrid pace of investing from the US-centric venture capital industry.

If we extrapolate five years from now into 2026 and assume that these trends continue, then we can posit that ROW will continue to gain in share and comprise of, say, 38% of the global unicorns. This figure is probably a very conservative one given the trends I highlighted earlier regarding the acceleration of US VC capital flowing outside the US. The chart below shows how this might play out in the coming years.

Rest of World is steadily increasing its share of global unicorns

On a percentage basis, this figure sounds relatively modest — another five percentage points in five years. But on an absolute number basis, the implications are profound. If we assume that the rate of growth of unicorns continues at a similar pace in the next five years as it has over the last five years, we will see a total of nearly 4,000 unicorns in December 2026. If the ROW share of unicorns does indeed increase to 38%, then the total number of unicorns from the rest of the world will be an astonishing 1,493 — an increase of 1,233. If the share actually accelerates a bit, then the total number of new international unicorns outside of China will equal that of the US — despite the fact that US VCs manage two-thirds of the industry’s capital.

Looking ahead, the number of new unicorns from Rest of World could outpace the US in the next five years

Unicorns or Bunnies?

The bottom line? In the coming years, US VCs — even small, niche ones like my firm, Flybridge — are learning to invest globally. As we make our first few investments in any individual country or region, our networks expand, our contextual awareness improves, and our comfort level for making the next new investment increases. As a result, international entrepreneurs are going to be able to attract US VCs in the coming years more easily than ever before.

And one final prediction — for those pessimists who think the unicorn herd is going to thin out in the coming years, think again. The unicorns are going to multiply so quickly in the next five years that we may start to think of them more like bunnies.

A young VC, when his hair was less gray, hanging with the former Fed Chair

Many people forget that former Fed Chair Alan Greenspan’s now-famous reference to “irrational exuberance” was in 1996. At the time, he asked the provocative question: “How do we know when irrational exuberance has unduly escalated asset values?”

Investors are asking themselves this poignant question over and over again in recent months. When my Flybridge partners and I were preparing for this week’s annual investor meeting, we stepped back to reflect on how to balance the obvious exuberance we are seeing in the market with our robust optimism that there are sound, fundamental reasons behind this exuberance. We came up with the phrase, Rational Exuberance, as the best way to capture the moment that we find ourselves in. Yes, valuations have soared and we VCs are all paying more as we construct our portfolios. Yet, like other top firms in the industry, we are realizing that for our best companies, the scale of market opportunities has proven to be much larger than previously anticipated. Our entry price may be 30–50% higher, but we are investing in companies that are exhibiting 3–5x higher exit potential. That’s a trade we will take over and over again. Let me unpack why we — and many others — have come to this conclusion.

Rational Exuberance?

Valuations have soared to a record high in the last few years, particularly in the public markets. For example, the NASDAQ has increased 105% in the nineteen months since the COVID-19 crisis in March 2020. And from the public markets, those valuations have cascaded down to the later stage private market, where capital is pouring in at record levels.

As a result, the rise in startup valuations — particularly later stage startups — is dramatic. The chart below, drawn from Pitchbook’s latest data set, shows the sharp increase in the last two years. Later stage financing valuations have grown so sharply and on such a large scale that the magnitude of the change in valuations at Flybridge’s stage — the seed stage, labeled here the Angel stage by Pitchbook — is imperceptible.

But everyone in our small corner of the early-stage market has also seen substantial valuation increases. When we analyzed our seed-stage deals across three recent cohorts — 2017–2018, 2018–2019, and 2020–2021 — we saw that despite being located outside the ridiculously competitive Silicon Valley (our offices are in NYC and Boston), our post-money entry valuations have grown 56% and 33%, respectively (see chart below).

Interestingly, each of these cohorts raised more capital. The average seed round size for our portfolio companies in 2016–2017 was $1.7M while it grew to $2.6M in our 2018–2019 cohort and then $3.3M in our 2020–2021 cohort. Entrepreneurs are taking advantage of the higher prices to raise more capital in the seed round and thus make more progress before raising their series As — leading to dramatically larger series As at dramatically higher valuations. Crunchbase recently reported that the average Series A round has increased from $6M to $18M.

Come on Get Higher!

Why are valuations rising across the board across all segments?

The obvious answers are Economics 101 (thanks, Alan) and well covered in the daily newspapers: capital is chasing yield in a low interest rate environment, more capital drives up prices (simple supply and demand) and at the same time, when later stage and public investors do their future value math for growth companies, low-interest rates result in higher future value calculations — thereby valuing growth even more.

The less obvious answers are what we are seeing on the ground as we work with our companies day-to-day. First, technology innovation is affecting and disrupting the entire $23 trillion US GDP. We used to focus on a little small corner of the market called the IT industry. Today, every company is a technology company, and every industry — from healthcare to financial services to retail to real estate — is being disrupted.

Second, with a nod to Thomas Friedman, the world has gotten flatter. Global smartphones have now reached over 80% of the world’s population up from 25% just six years ago, increasing the potential market for all of our companies. And, finally, as we study technology adoption patterns, we are seeing a fundamental shift to more rapid, earlier adoption of new products and services.

I have written in more detail about this phenomenon that we are seeing of faster technology adoption, framing the situation in the context of Geoffrey Moore’s canonical book from 30 years ago, Crossing the Chasm. In short, every business on the planet is realizing that they need to be an early adopter and embrace new technologies or they will be disrupted — think Blockbuster and Barnes & Noble. And every consumer has been trained to rapidly embrace new apps that make their lives easier and richer. As a result, the pace of technology adoption has quickened and the potential market size that startups can address in their early years — even if their product isn’t perfect and their organization is still nascent — has dramatically expanded. That’s why a young infrastructure company like our portfolio company MongoDB can count over half of the Fortune 500 as their customers at the time of their IPO a number of years ago.

All of this is leading to our conclusion that market sizes are proving far, far larger than we had ever imagined — surpassing our most optimistic forecasts and prognostication.

Faster Than a Speeding Bullet

We can see these trends play out across the entire tech ecosystem. For example, by looking at the revenue growth rates that the Big Five tech companies reported last quarter. Each of these companies, worth over $1 trillion, is supposedly operating mature businesses at scale, and yet they are still reporting growth rates in the 20–60% range — as if they were VC-backed startups.

Speaking of VC-backed startups, Bessemer’s recent report on the top 100 private cloud companies was also astonishing. Their analysis showed that on average, the revenue growth rates for these large private companies — as an entire cohort — have risen to 90% year over year while the top quartile is growing 110%. Again, these are large-scale companies defying the “law of large numbers”.

Recreating the Entire GDP of China…in 5 Years

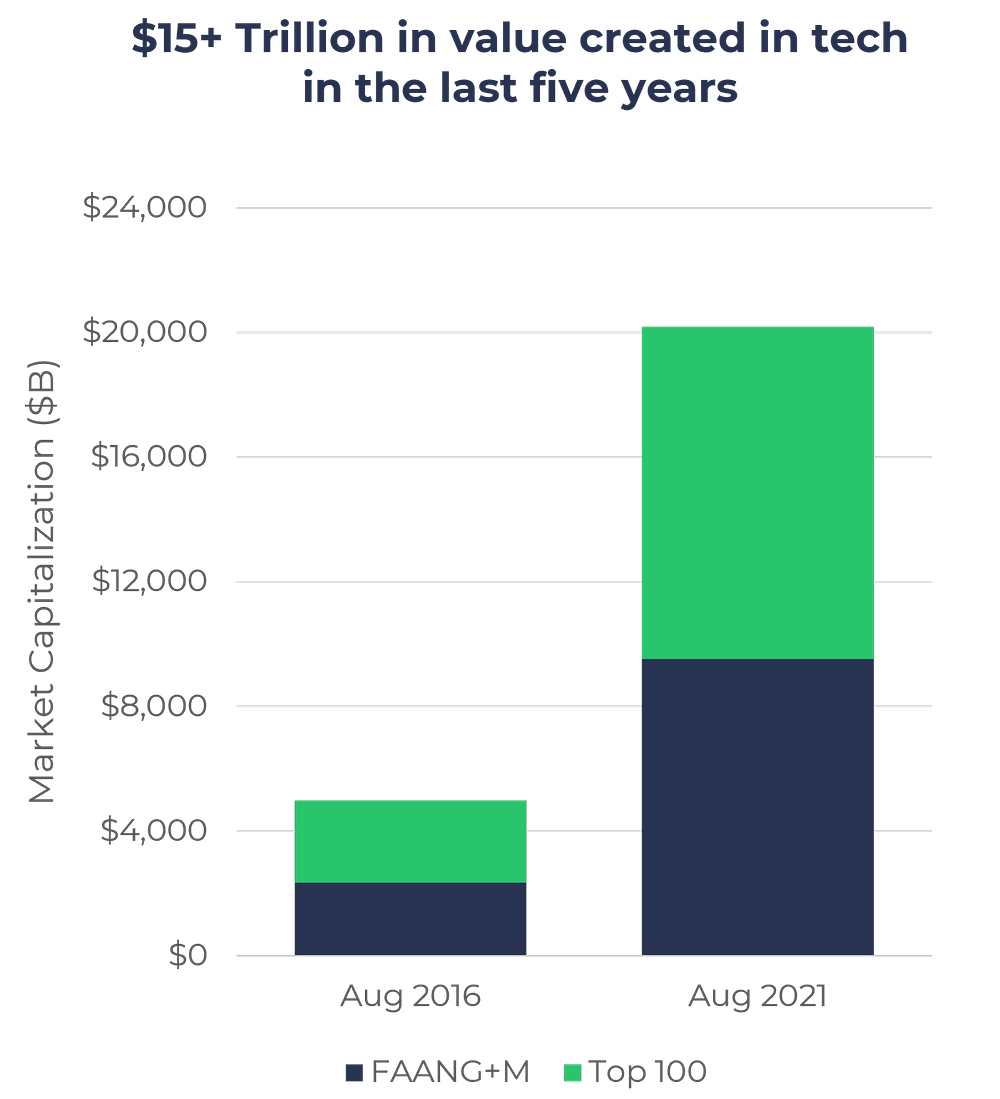

As noted, these powerful forces driving accelerating revenue growth as a result of very favorable underlying market conditions and rapid adoption curves have led to unprecedented increases in valuation. We wanted to quantify this and so looked at the handful of Big Tech companies mentioned earlier along with the top 100 next most valuable tech companies and compared their change in market capitalizations from five years ago to today.

Even we were astonished to see the result. That cohort of companies has grown from $5 trillion to $20 trillion — an increase of $15 trillion. That is a staggering amount of value creation in tech in the last five years. To put that figure in perspective, $15 trillion is equivalent to the entire GDP of China.

Further, in our analysis of the top 100 most valuable companies, we noticed that 27 of these companies are newly public — that is, they were still private companies five years ago, invisible to the public markets and operating solely in the VC market.

Speaking of the VC market, these forces and favorable conditions have also led to the substantial growth in the number of unicorns (i.e., companies who have private valuations > $1 billion). Specifically, the number of unicorns has grown from 39 in 2013 to 842 today, a cohort worth nearly $3 trillion. Add that to the public growth and you have $18 trillion of market value creation in tech in the last five years.

Conclusion: Let the Good Times Roll

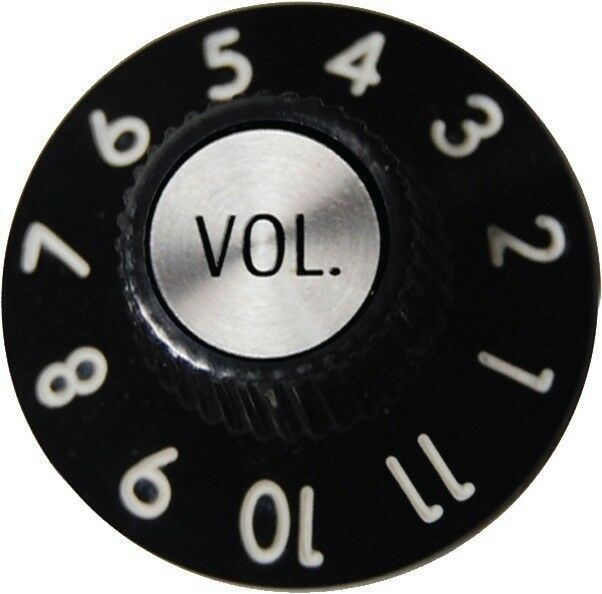

Thus, if we pull the camera back on the environment, it is clear it has been an exuberant period of time — but there are a good number of rational underpinnings to that exuberance. And with the advent of Zoom investing and remote work, the points of friction have been dramatically reduced and we are all operating at a velocity of 11.

No one can predict whether future public valuations and multiples will continue to soar or if we are heading into a market correction. But as I talk to my peers in the industry, there is universal confidence that we participants in startupland are on the right side of important secular trends. The shift towards global technology adoption for enterprises and consumers is a trend that is simply not going away. The rate of adoption of smartphones, apps, cloud, AI, data proliferation, and all the investment sectors that we and others have operated in successfully for the last two decades continue to dramatically grow on a global scale.

As a result, VC investors are finding our opportunity set to be as attractive as it has ever been in history. Of course, if everyone realizes that — and everyone does — more capital is coming. A lot more. I may not have Alan Greenspan’s economic wisdom or hubris about an ability to predict the future, but of that last point, I am quite certain.

special thanks to my colleagues for their insights and input — Matt Guiney, Chip Hazard, Julia Maltby, Justin Mead, Jesse Middleton, and Anna Palmer — as well as Asha Tanwar for her expert research and analytical assistance.

A few months ago, I wrote about the ridiculous increase in velocity that we are seeing in the venture capital market in my post, Velocity and Venture Capital: 11. Now that summer is upon us, I want to reflect on the subtle value of slowing down, particularly from the standpoint of an entrepreneur.

Summer has always been a time to take a breath and slow down. Now that the United States is entering into a post-pandemic phase, we have yet another reason to take things a bit slower and stop obsessing over efficiency and speed. One of my more popular tweets in the last year was:

I was reminded of the value of slowing down in the last few days by one of my founders who is in the midst of closing a massive financing at a “unicorn” valuation. The company is on a tear, having grown 30x in revenue year over year. In a moment of candor, he confided to me, “I hope the new investors will let me slow down. We need to make sure we are building for scale and to do that, I need to be more deliberate in our growth.” Like the tortoise in the famous Aesop’s fable, sometimes we need to proceed slowly and steadily to win the race.

Here are a few of the benefits of slowing down, and where entrepreneurs may want to focus their energies this summer:

Solidify Your Scalable Team. CEO coach Marshall Goldsmith has a brilliant book, What Got You Here Won’t Get You There, about successful executives hitting points of friction as they grow, requiring changes in their behavior in order to continue to succeed. I often coach my entrepreneurs to assess their teams with a similar lens. The team that got you here may not be the team that will get you there. Take the time to consider team additions, upgrades, and perhaps coaching or facilitation to ensure you have the right aligned senior team that is ready, willing, and able to scale to the next level.

Think Different. When you’re running a fast-growing company, with all the execution demands and details involved, it is hard to take the time to be creative. Take the time this summer to do some offsites (yes, in person!) and brainstorm with your teams regarding the nonlinear growth opportunities that might be available to you. Consider transformative acquisitions, partnerships, new product launches, or international expansion in ways you might not have had the time and space to think through.

Pay Down Your Organizational Debt. Every fast-growing startup incurs debt along the way. Those forms of debt include technical debt (paying the price for historically putting off building a robust platform in order to meet short-term customer needs), process debt (taking shortcuts for the sake of expediency to get things done without stopping to make core business process robust and repeatable), and cultural debt (not investing in the culture and values because you’re so busy trying to avoid drowning in work and the demands of the market). Take the time this summer to pay down all forms of organizational debt. Don’t let the excuse, “we haven’t had the time” stop you from cleaning up some of the messes that were left in the wake of past sprints.

Build Enduring Relationships. Covid has made it hard to build authentic, deep relationships. Zoom makes everything more efficient, but more transactional. This summer, take the time to hone in on a few important relationships and make the effort to meet up face to face, spend unscheduled long stretches of time, and (gasp) just hang out. Personally, I’m terrible at slowing down. Zoom has brought out the worst of my tendencies in this regard and so am keen to heed my own advice here!

In Jim Collins’ book, Built to Last, he writes about the playbook for building an enduring company. Spoiler alert: slowing down to focus on team, culture, organizational design, business model and continuous improvement are all a part of the formula. So take a breath this summer and redouble your commitment to building a company and business that will endure.

When I was at Open Market in the 1990s, our CEO gave out the recently published book, Crossing the Chasm, to the executive team and told us to read it to gain insight into why we had hit a speed bump in our scaling. We had gone from 0 to $60m in revenue in four years, went public at a billion-dollar market cap, and then stalled. We found ourselves stuck in what author Geoffrey Moore called “The Chasm” where there is a difficult transition from visionary, early adopter customers who are willing to put up with an incomplete product and mainstream customers who demand a more complete product. This framework for marketing technology products has been one of the canonical foundational concepts to product-market fit for the three decades since it was first published in 1991.

Recently, I have been reflecting on why it is that we venture capitalists and founders keep making the same mistake over and over again — a mistake that has become even more glaring in recent years. Despite our exuberant optimism, we keep getting the potential market size wrong. Market sizes have proven to be much, much larger than any of us had ever dreamed. The reason? Today, everyone aspires to be an early adopter. Peter Drucker’s mantra, innovate or die, has finally come to pass.

A glaring example in our investment portfolio of market sizes is database software company MongoDB. Looking back at our series A investment memo for this disruptive open source, no SQL database startup, I was struck that we boldly predicted the company had the opportunity to disrupt a sub-segment of the industry and successfully take a piece of a market that could grow as large as $8 billion in annual revenue in future years. Today, we now realize that the company’s product appeals to the vast majority of the market, one that is forecast to be $68 billion in 2020 and growing to approximately $106 billion in 2024. The company is projected to hit a $1 billion in revenue run rate next year and, with that expanded market, likely has continued room to grow for many years to come.

Another example is Veeva, a vertical software company initially focused on the pharmaceutical industry. When we met the company for their Series A round, they showed us the classic hockey stick slide, claiming they would reach $50 million in revenue in 5 years. We got over our “is the market big enough?” concern when we and the founders concluded they could at least achieve a few hundred million in revenue on the backs of pharma and then expand, as the company’s initial name indicated, to other vertical industries from there. Boy, were we wrong! The company filed their S1 after that fifth year showing $130 million in revenue and today the company is projected to hit a $2 billion in revenue run rate next year, all while still remaining focused on just the pharma industry.

Veeva was a pioneer in “vertical SaaS” – software platforms that serve niche industries – which in recent years has become a popular category. Another vertical SaaS example is Squire, a company my partner Jesse angel invested in as part of a pre-seed round before he joined Flybridge. When Jesse told me about them — a software company dedicated to barber shops — I thought, “Nice. Sounds like a niche opportunity to get to $10+ million and then sell for a good profit.” When they graduated from startup accelerator YCombinator several years ago, they were barely able to scrape together a $1 million seed financing. As co-founder and CEO Songe LaRon shared with me, “Total available market size was the Achilles heel of our business in the eyes of investors.” Those prospective investors who passed ended up being dead wrong. Today, the company is doing hundreds of millions of dollars in transaction volume. A few months ago, Squire announced a $45 million financing at a valuation of $250 million.

I can’t resist one more example that brings this point of expanding market sizes home – the compound annual revenue growth rates (CAGR) over the last three years for the largest tech companies in the world have continued at a torrid pace, as noted below:

Amazon: 30%

Facebook: 29%

Google: 18%

These companies are mature businesses with hundreds of billions of dollars in revenue, and yet they are still growing at CAGRs of 20-30% per year!

Why is it that in recent years, wild-eyed optimistic VCs and entrepreneurs keep under-shooting market size across the tech and innovation sector? Upon reflection, I think there are two problems: the Chasm is outdated and Marc Andreessen was right about software eating the world.

Market Size Definitions: TAM and SAM

To understand our persistent problem with market size forecasting, let’s first deconstruct what is Total Available Market (TAM) size. A company’s TAM is a simple formula of the number of potential customers multiplied by the total revenue per customer. TAM is a snapshot of the total dollar potential in the entire market.

Serviceable Addressable Market (SAM) is the portion of the market that is an actual fit for your product or service. For example, the total global database market is $150 billion. That’s the TAM. But the SAM for MongoDB is the portion of the database market that is a fit for their particular approach, no SQL. That is projected to be $22 billion in a few years. That’s the SAM.

Typically, we are trained to think that only a portion of the SAM is obtainable within any reasonable window of time because of The Chasm and so the trick is to focus on attacking and expanding the SAM.

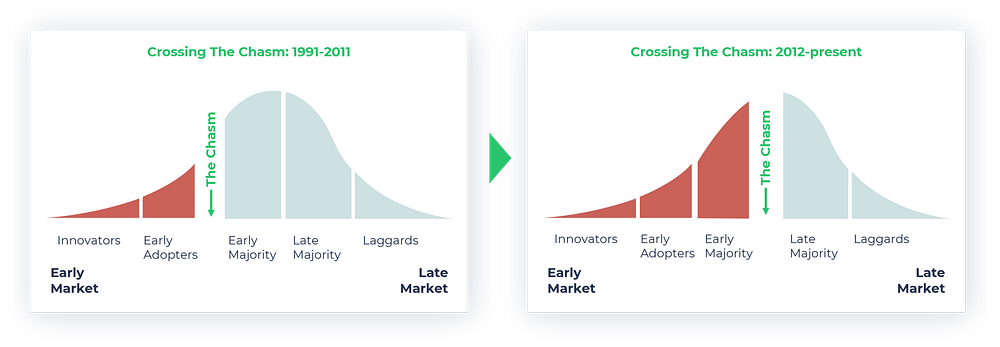

The Chasm: 1991-2011

In characterizing why it was so hard for technology companies to introduce discontinuous innovations, Moore framed a technology lifecycle that described different types of customers. He observed, “Our attitude toward technology adoption becomes significant any time we are introduced to products that require us to change our current mode of behavior or to modify other products and services that we rely on.”

He divided up the different customer groups based on their psychographic profile and attitude towards technology adoption into a bell curve: innovators, early adopters, early majority, late majority, and laggards. In between the innovators and early adopters, there is a small chasm. In between early adopters and the early majority is a larger chasm. The chasm, Moore explains, is because early adopters are open to change; they aspire to “get a jump on the competition…and expect a radical discontinuing between the old ways and the new.” In contrast, the early majority is “looking to minimize the discontinuity with the old ways. They want evolution, not revolution.”

The image below from Moore’s book lays out the small and large chasms in the transition across all of the market subdivisions nicely.

The Chasm: 2012-present

In recent years, this model for technology has broken down. The reason, I submit, ties to Marc Andreessen’s famous Wall Street Journal article, “Why Software Is Eating the World.”

Marc correctly voiced what many of us in the industry felt when he wrote, “We are in the middle of a dramatic and broad technological and economic shift in which software companies are poised to take over large swathes of the economy.”

Over the last 10 years since that article was written, businesses now finally “get it”. And this year, in particular, the pandemic helped accelerate a global appreciation that digital innovation was no longer a luxury but rather a necessity. As such, companies could no longer wait around for new innovations to cross the chasm. Instead, everyone had to embrace change or be exposed to an existential competitive disadvantage.

Using Moore’s framework and combining it with Andreessen’s observation, I would argue that the early market overall (which includes innovators, early adopters, and the early majority) has grown substantially larger than before and, further, that due to competitive necessity, the early majority has embraced change and jumped across the chasm. And the portion of the market that the late Majority and laggards represent is smaller than ever before. A pictorial description of this phenomenon can be seen below.

This corporate imperative to embrace change, which extends to consumers who are more comfortable adopting technology products than ever before, coupled with the fact that software has become a more and more valuable portion of the world, is what is driving surprisingly massive market sizes.

The best companies are able to take advantage of this accelerated adoption curve by launching additional products once they have established an initial market toehold. Those additional products serve to increase their SAM – and do so at a rapid pace as they fly through the customer adoption process. Veeva, for example, today has 35 different products targeted at the sales and marketing function, regulatory affairs, and clinical. Squire, for example, has built upon their initial scheduling product to include payments and plan to launch additional modules to support banking and the online ordering of supplies. It helps that the rise of the cloud and advancements in software development tools and techniques are such that more rapid product development than ever before can be achieved. And, as noted above, companies are now more primed for rapid software adoption than ever before.

Conclusion

Looping back to our market size definitions, “software eating the world” has dramatically expanded the TAM while also catalyzing a compressed technology adoption lifecycle, which has dramatically expanded the SAM.

This trend towards rapidly growing and ever-expanding market sizes, and their signal as a leading indicator towards value creation, represents a promising development in our innovation ecosystem. Faster adoption cycles have a positive feedback loop on innovation: the more companies and consumers adopt new technologies, the more entrepreneurs can get funded to build the next new thing.

As we emerge from the pandemic, it’s the common casual question that many of us receive when we reconnect with our friends. I find I am struggling to answer it concisely. In my over twenty-five years in the startup and venture capital (VC) industry, I have never seen anything like this moment that we are in. To answer this friendly inquiry in as clear and open a manner as possible, the only word that comes to mind is velocity.

As everyone who took high school physics knows, velocity is the rate of change of an object’s position over a period of time as compared to a frame of reference. Entrepreneurs and VCs have a common historical frame of reference: we are all accustomed to moving quickly and dynamically in our collective journey to fund and build innovative, ground-breaking companies. That collective journey has created a series of routines and common practices over the many decades since the first venture capital firm, ARD, invested in Digital Equipment Corporation in 1957.

What’s changed in this pandemic is that the velocity of our activity has dramatically increased due to the systemic removal of any modicum of friction that might have existed in “the old days” up until March of 2020.

Startup Fundraising Process: 1957-2020

To get a sense of how this increased velocity is happening in practice, let me deconstruct the typical fundraising process for the last 60 years of venture capital and startups:

Entrepreneurs set up meetings with VCs and travel to their offices in SF, NYC, and/or Boston (this business is profoundly concentrated, with 85% of total assets under management in the US concentrated in just three states: California, New York, and Massachusettes).

A week or two later, follow-up meetings take place at the VC offices for broader exposure amongst the partnership and management teams.

Then, entrepreneurs host investors in their offices to provide the opportunity for a deeper dive into the business and a tangible sense of the culture as well as an opportunity to meet key executives.

Upon passing further due diligence to everyone’s satisfaction, the management team presents to the entire VC firm on Monday during the weekly partners meeting (which always, always happens on Mondays).

If the investment decision is made, negotiations on deal terms commence, and after some back and forth over a number of days and additional face-to-face meetings, term sheets are issued and signed.

Lawyers from both sides are retained to negotiate the definitive investment agreements.

Definitive agreements are signed, the investment is closed and money is wired.

Entrepreneurs would typically meet with 20-30 firms in order to secure 2-3 term sheets and select their chosen partner. This process typically would take 3-6 months end-to-end simply due to the logistics of multiple rounds of meetings, travel, scheduling, and negotiations. Hence, when we are coaching our entrepreneurs regarding “how long should I plan to be fundraising?”, 3-6 months is prudent having 6-9 months of cash cushion gives you a little wiggle room.

Startup Fundraising Process: 2020-2021

When covid hit, everyone’s world turned upside down and remote. VCs and entrepreneurs have adapted particularly quickly. As a result, the fundraising process for today’s entrepreneurs goes as follows:

Hold twenty to thirty Zoom meetings, each in 30-minute increments, over the course of a handful of days to meet prospective investors.

For deeper dives, 60 or 90-minute follow-up meetings are scheduled with a broader set of VC partners at the prospective firm along with various members of the management team — each of whom seamlessly Zooms in for their relevant portion of the meeting.

Like Flybridge, many VC firms have shifted their model from weekly Monday morning meetings to multiple meetings per week — after all, with zero travel and infinitely flexible schedules, it’s easy to coordinate the entire investment team’s calendars and hold more frequent, smaller time slots to meet teams and discuss investment opportunities.

Deal documents are now completely standardized and simple. For those of us who invest in the early stages, SAFE notes are the “currency of the realm,” which means there is very little to negotiate once an investment decision is made except for price and amount.

Any possible points of friction — meeting the entire partnership, meeting other members of the management team, negotiating deal elements, forming a full investment syndicate — have been eliminated or sharply reduced, easily squeezed in during the course of a day full of remote meetings over Zoom.

As a result of this reduced friction, fundraising — even for large later-stage companies — takes only a few weeks. Thus, velocity has dramatically — in many cases, breathtakingly — increased.

Some Data

Pitchbook recently released their Q1 2021 report, demonstrating the frenetic pace that everyone in the technology and innovation world is experiencing. Investors deployed $69 billion into nearly 4,000 VC-backed companies in Q1, an increase of 93% in capital deployed in just one year. The amount of capital being deployed, never mind the surge of IPOs and SPACs, is simply dizzying. If you take the estimated early-stage deal count in Q1 2021 1,170 and annualize it to 4,680, it represents a 50% increase from 5 years ago.

To see this graphically, look at the chart below (again, using Pitchbook data). I took the annual overall deal value in Q1 and simply annualized it and chart it in comparison to the last 15 years. At a more granular level, the quarterly data shows that the climb in deal value has been dramatic since the pandemic.

A lot has been written about the rise of SPACs, another financial instrument that makes more capital available to entrepreneurs. The chart below shows that the SPAC market raised record capital in just one quarter as compared to previous years. Again, this surge would only be possible with a surge in velocity and the dramatic reduction of deal friction.

As venture capitalist, Everett Randle put it in an insightful blog post about Tiger Global’s strategy of high-velocity capital deployment (which is being replicated by many aggressive growth stage investors), “[Tiger and other fast-moving VC firms] have turned the velocity dial to 11.”

Implications

There are many obvious upsides to this increase in velocity, but there are many downsides. Forget that VCs and entrepreneurs are working harder than ever (whine away, my friends — I hear the violin music now). What really concerns me is the sloppiness that results in increased velocity. Faster due diligence, faster decisions, and fewer opportunities to slow down and build authentic, trust-based relationships can be dangerous when there are bumps in the road. The faster your velocity, the bigger an impact those speed bumps make on you and the organization.

Further, the famous “fraud triangle” of opportunity, incentive, and rationalization suggests this surge in velocity could yield both a surge in underlying incentive and opportunity. Fraud in entrepreneurial settings can range from the obviously illegal (see: Theranos and uBiome) to the slightly exaggerated.

When we are all vaccinated and back to meeting face-to-face, this unsustainable velocity will surely slow down. Right? Until then, everyone is operating at “11”.

Picking the right place to launch your career is more important than ever

A year ago, in the wake of the pandemic, finding a growth-stage startup for graduating students hungry to dive into the startup community was about as hard as could be imagined. This year, thanks to arguably the greatest tech and innovation boom in history, graduating students have an abundance of opportunities to productively start their careers.

Each spring, I provide a comprehensive list of exciting, growing, hiring startups that are worthy of consideration as places to start or continue a career in StartUpLand. I try to be as objective as possible in creating the list, leveraging insider knowledge and input from VC and entrepreneur friends regarding who has real momentum. The objective criteria for being on the list is is a mix of fundraising (typically > $20m in the most recent round), scale (typically > 100 employees), momentum (typically growing users or revenue > 50%/year), and hiring (typically growing headcount > 50%/year, including a number of entry-level positions that would be a fit for recent college or business school graduates).

I try to include a few international startups each year, thanks to my VC friends in startup hubs like China, India, Israel, South America, and Western Europe. Pitchbook data is less reliable outside the US so I am particularly grateful to those who shared their local market insights.

Before listing the companies, I suggest checking out two of my posts where I give more detailed advice on how to select the right company for you and position yourself to secure a job — a playbook that is more important than ever in this competitive environment:

Once you have reviewed this framework for deciding what you’re looking for, review the nearly 400 companies (276 US, 115 International) below. As usual, the list is organized by location. Even in an era of remote work, I advise my students (borrowing a bit from David Brooks) to select a geographical particular community to invest in and contribute to over the long term. Similar to last year, the list is also organized by sector and we created an Airtable to make it easy to navigate.

I’m sure I made many mistakes and omissions and I thank you in advance for any feedback you might have — the wisdom of the crowd definitely makes this list better. Very special thanks to the indomitable Shreyas Nair of Harvard Business School and Sequoia, who spent countless hours helping me sort and resort the list. Without further ado:

Disclosure: Among the listed companies, the following are Flybridge portfolio companies — Bowery, Chief, Codecademy, FalconX, Imperfect Foods, Infracommerce, MadeiraMadeira, NS1, and Splice

2020 Has Been a Year of Incongruous, Unprecedented Wealth Creation

Inspired by Bill Gates, who calls the practice his annual “Think Week”, I try to read a few intellectually stimulating books during the final two weeks of each calendar year. This year, my book choices ranged from racial inequality (Caste: The Origins of Our Discontent), history (China and Japan: Facing History by my Uncle Ezra Vogel, a scholar and mensch who suddenly passed away a few weeks ago at 90), autobiography (Obama: A Promised Land), and fiction (Philip Roth’s Nobel Prize-winning American Pastoral). Added to this year’s mix was a book my 18-year-old son insisted I read as he recently declared it is his favorite book of all time: Hermann Hesse’s Siddhartha, a novel about the journey of a young Indian boy who gives up a life of privilege to search for truth, leading him to become the Buddha.

It was a nice respite from the mess that was 2020. In wrapping up our year and looking ahead, many pundits and politicians have emphasized the four crises that we face heading into 2021: the pandemic, racial inequality, climate change, and a wounded economy.

Incongruously, in the face of these four crises, the stock market ended the year at a record high, largely driven by a surge in tech stocks. In fact, the hidden secret of 2020 is that it has been a spectacular year for wealth creation. A review of the numbers shows the staggering amount of new wealth that was created during this horrific year of death and disruption. A few examples of note:

The collective wealth of America’s 651 billionaires grew $1 trillion since the start of the pandemic: from $3 trillion to $4 trillion.

Jeff Bezos and Elon Musk alone have seen a surge of $200 billion in new wealth.

The IPO market had a banner year. Three recently public companies alone — Airbnb, DoorDash, and Snowflake — are now worth over $210 billion in value.

The combined market capitalization of Bitcoin and Ethereum grew from $140 billion to over $680 billion, a gain of $540 billion in value in just one year for their holders.

Even in my hometown of Boston, the degree of wealth creation has been stunning. Just look at five companies that have benefited from the pandemic’s digital acceleration and life sciences boom: DraftKings, Hubspot, Moderna, Thermo, and Wayfair. In March, the combined market capitalization of these five companies was approximately $130 billion. At the market close on 12/31/20, the combined market caps had soared well over 100% to nearly $300 billion, creating $170 billion of new wealth for their executives and shareholders.

All of this in a year where the country’s GDP is forecasted to contract by almost 4% and unemployment is nearly 7%. Economists and historicans will try to deconstruct this disconnect between Wall Street / Silicon Valley and Main Street, between the Winners and Losers, for years to come. What I want to reflect on, though, is what are the implications of this unprecedented situation.

How will this staggering amount of new wealth be applied in the midst of our four parallel crises? What will these few thousand individuals do with their newfound wealth in the coming year? Will we slip into a greater sense of malaise over the vast inequality and unfairness in our society?

Looking ahead, I predict three things will happen:

A surge in philanthropy. I believe we are about to enter a golden age in philanthropic giving. The wealthy feel both a strong sense of obligation and a dash of guilt. The popularity of the billionaire’s Giving Pledge that Warren Buffett and Bill started is a strong indication of that — more are joining on (seven new ones signed up this year alone) and these (mostly) men and women are beginning to reach an age where they are ready to focus on their philanthropy. Jeff Bezos’ ex-wife MacKenzie Scott, quietly donated over $4 billion alone to charities in the final months of 2020. We are entering a golden age for nonprofits.

A surge in money in politics. It’s hard to imagine more money in politics, yet that is what is about to happen. Every one of these billionaires and multi-millionaires has an agenda or cause they are passionate about — fighting climate change, protecting democracy, reforming public schools — and therefore they will seek to influence policy, and the politicians who make that policy, at an unprecedented level. The Georgia Senate race has seen well over $300 million raised, making them the most expensive and second most expensive seats in history. Get ready for more of the same: so long as money can continue to influence policy, money will influence politics (or is it the other way around?). Anand Giridhadaras covers this well in his book as well as this NY Times article on the Billionaire’s Election.

A return to populist rage. Occupy Wall Street gave us a taste of it but I believe we are going to see more protests and populism tied to inequality in addition to people taking to the streets to protest against socialism (from the right) or racism (from the left). Occupy Wall Street was sparked by a single unpredictable incident — as was the Arab Spring, as were the George Floyd protests — and so we may see another unpredictable incident lead to another round of protests in 2021. When President Obama admonished the CEOs of banks in a 2009 White House meeting that he was the only one standing between them and the pitchforks, it was a foreshadowing of what can happen when the American people no longer believe their institutions as being fair. The handling of the pandemic, the vaccine distribution, and the way trillions of dollars are being pumped into the economy are all ingredients that suggest we may see an unpredictable ignite populist rage in America over inequality in 2021.

2021 will be defined by what we as a society do with this newly created wealth — how it is divided up and deployed? In a year where our system of both capitalism and democracy have been challenged to their core (something I was deeply worried about this time two years ago, as described in my Think Week blog post of 2019), I hope we can figure this one out. I am an optimist at heart and so will be rooting for all the good that can come from this — and hoping that our civic and business leaders are thinking deeply about these critical questions heading into the new year.

Over the last few weeks, I was inspired to re-read Zen and The Art of Motorcycle Maintenance, a book I read in my late teens and remember enjoying.

At the time, I embraced its emphasis on Quality (hard to define, easy to discern) as an organizing mantra for living a purposeful life. The book was published in the 1970s at a time when many young people were waking up from the hangover of the 1960s and feeling aimless and unfocused. What was the meaning of life and how should a good life be lived? Author Robert Pirsig does a brilliant job trying to address these big questions with a ranging review of Buddhism, Socrates, Plato, Kant, and other philosophers all told through the prism of an autobiographical journey on a motorcycle through the great expanse of the West with his young son. It has since become the best-selling philosophy book of all time.

Reading Zen decades later, though, gave me a new perspective on the book and its lessons for the art of startup building. Pirsig spends time highlighting the limitations of the scientific method and those limitations are ones that I’ve been thinking about recently in the context of startups.

The scientific method is a process for experimentation that rests on the belief that hypotheses should be sharply defined and then rigorously tested through well-constructed experiments. Eric Ries popularized applying the scientific method to startups through his book, The Lean Startup.

At Harvard Business School (HBS), in both my class and the entrepreneurship department more broadly, we teach the importance of treating startups like experimentation machines. But HBS and other entrepreneurship programs and startup accelerators typically fall short when giving guidance as to how to determine which experiments to run. I have written in the past that for founders, test selection is all about strategic choices.

Entrepreneurs need to be thoughtful and disciplined regarding test selection, design, and prioritization. In short, entrepreneurs need to analyze their business model critically and select the tests that matter the most at each phase of their journey.

What is less well-understood is the process for determining which experiments to run and how to sequence those experiments. Given that founders have a discrete envelope of time and money before they need to produce positive results, experimentation selection is one of the most critical factors in startup success.

Pirsig speaks to this point in a more general sense. Written in the 1970s, Zen could not have anticipated the impact of his words on tech startups. But his argument applies beautifully to tech startups when he states that test selection must come from intuition. At one point late in the book he observes:

“You need some ideas, some hypotheses. Traditional scientific method, unfortunately, has never quite gotten around to say exactly where to pick up more of these hypotheses…Creativity, originality, inventiveness, intuition, imagination…are completely outside its domain.”

The problem for entrepreneurs, then, is how to build up this intuition. How should an entrepreneur best navigate the Idea Maze (a lovely metaphor from Chris Dixon)?

As with the elusive definition of Quality in Zen, the answer is subtle and not easy to deliver or communicate. We think we know how to identify a quality entrepreneur, a quality business plan, a quality consumer value proposition, a quality initial product, and a quality go to market plan. But is there a rule set that entrepreneurs can follow to know that they are on the right path? The sad answer is no. But founders can do a few things to help in developing that critical entrepreneurial intuition required to navigate the Idea Maze:

Customer Development. Immerse yourself in the customer problem set (i.e., perform deep customer development in the classically defined manner of Steve Blank and Four Steps to the Epiphany) to develop an intuition on the customer’s pain points to hypothesize compelling value propositions.

Domain Knowledge. Study the domain through both direct research (i.e., be an autodidact founder, defying the myth of Founder-Market Fit) and by surrounding yourself with domain experts to develop an intuition on the market dynamics and trends.

Strategy 101. Apply rigorous strategic thinking to the market dynamics, the value chain, substitutes and complements to develop an intuition on where profit pools may lie.

Built a Test Machine. Build an organization that is able to run tests rapidly and efficiently so that your testing throughput is faster than your competitors, building a startup organization that is a learning machine as well as an execution machine.

Follow these steps and, hopefully, you will find your path to Quality experiments, execution, and company-building.